Question: 3. Option Pricing a) Using a Binomial pricing model with 1-month steps, find the price of a 3-month American Call and a 3-month American Put

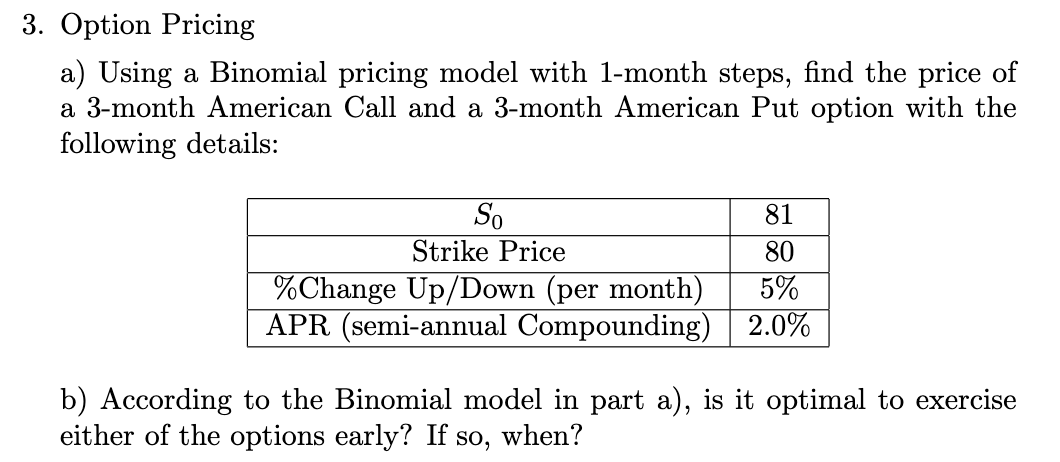

3. Option Pricing a) Using a Binomial pricing model with 1-month steps, find the price of a 3-month American Call and a 3-month American Put option with the following details: So 81 Strike Price 80 %Change Up/Down (per month) 5% APR (semi-annual Compounding) 2.0% b) According to the Binomial model in part a), is it optimal to exercise either of the options early? If so, when? 3. Option Pricing a) Using a Binomial pricing model with 1-month steps, find the price of a 3-month American Call and a 3-month American Put option with the following details: So 81 Strike Price 80 %Change Up/Down (per month) 5% APR (semi-annual Compounding) 2.0% b) According to the Binomial model in part a), is it optimal to exercise either of the options early? If so, when

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts