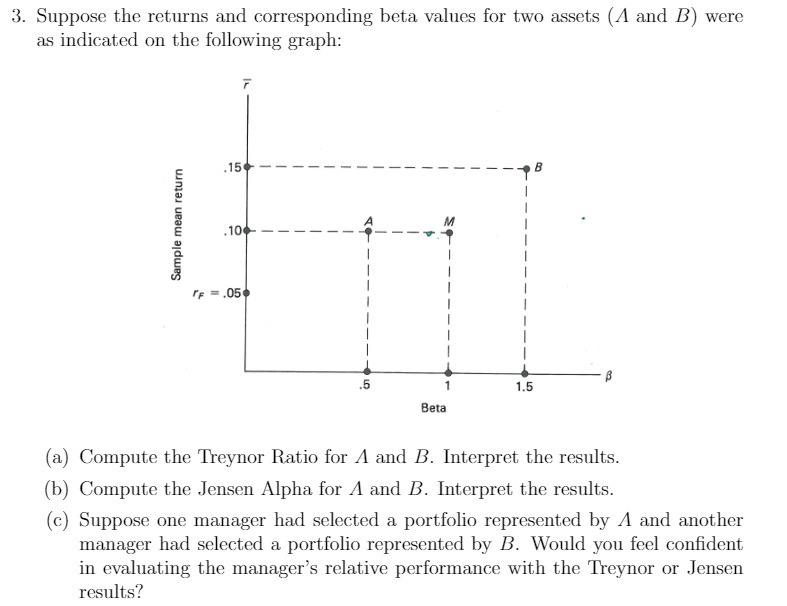

Question: 3. Suppose the returns and corresponding beta values for two assets (A and B} were as indicated on the following graph: ample mun return (a)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock