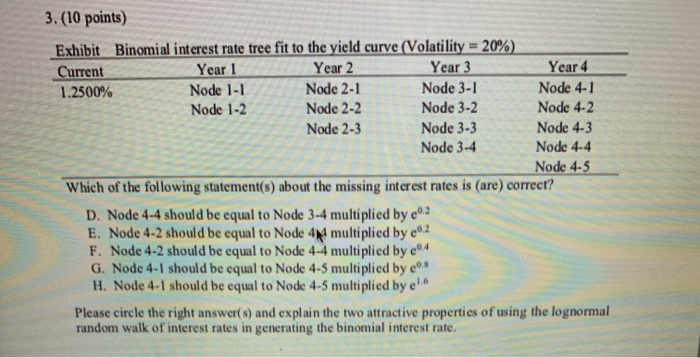

Question: 3.(10 points) Exhibit Binomial interest rate tree fit to the yield curve (Volatility = 20%) Current Year 1 Year 2 Year 3 Year 4 1.2500%

3.(10 points) Exhibit Binomial interest rate tree fit to the yield curve (Volatility = 20%) Current Year 1 Year 2 Year 3 Year 4 1.2500% Node 1-1 Node 2-1 Node 3-1 Node 4-1 Node 1-2 Node 2-2 Node 3-2 Node 4-2 Node 2-3 Node 3-3 Node 4-3 Node 3-4 Node 4-4 Node 4-5 Which of the following statement(s) about the missing interest rates is (are) correct? D. Node 4-4 should be equal to Node 3-4 multiplied by e02 E. Node 4-2 should be equal to Node 4 multiplied by e02 F. Node 4-2 should be equal to Node 4-4 multiplied by e4 G. Node 4-1 should be equal to Node 4-5 multiplied by e H. Node 4-1 should be equal to Node 4-5 multiplied by el. Please circle the right answer(s) and explain the two attractive properties of using the lognormal random walk or interest rates in generating the binomial interest rate

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts