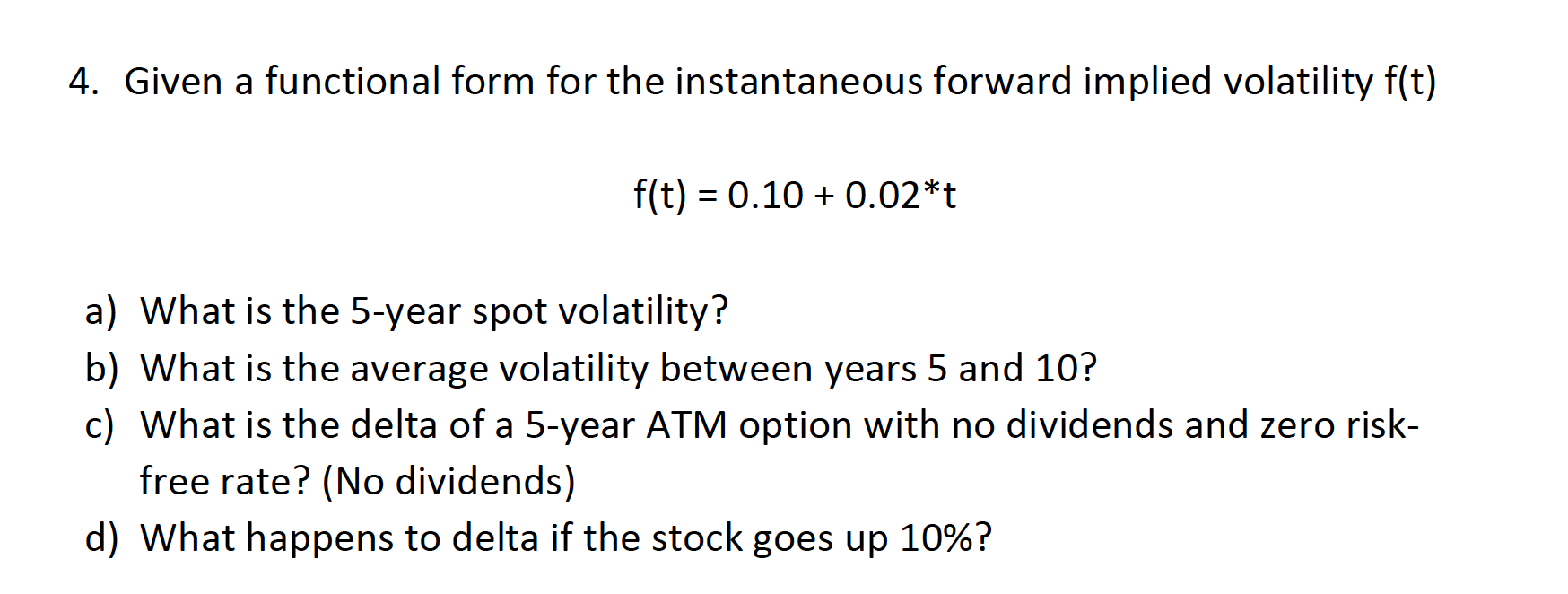

Question: 4. Given a functional form for the instantaneous forward implied volatility f(t) f(t)=0.10+0.02t a) What is the 5 -year spot volatility? b) What is the

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock