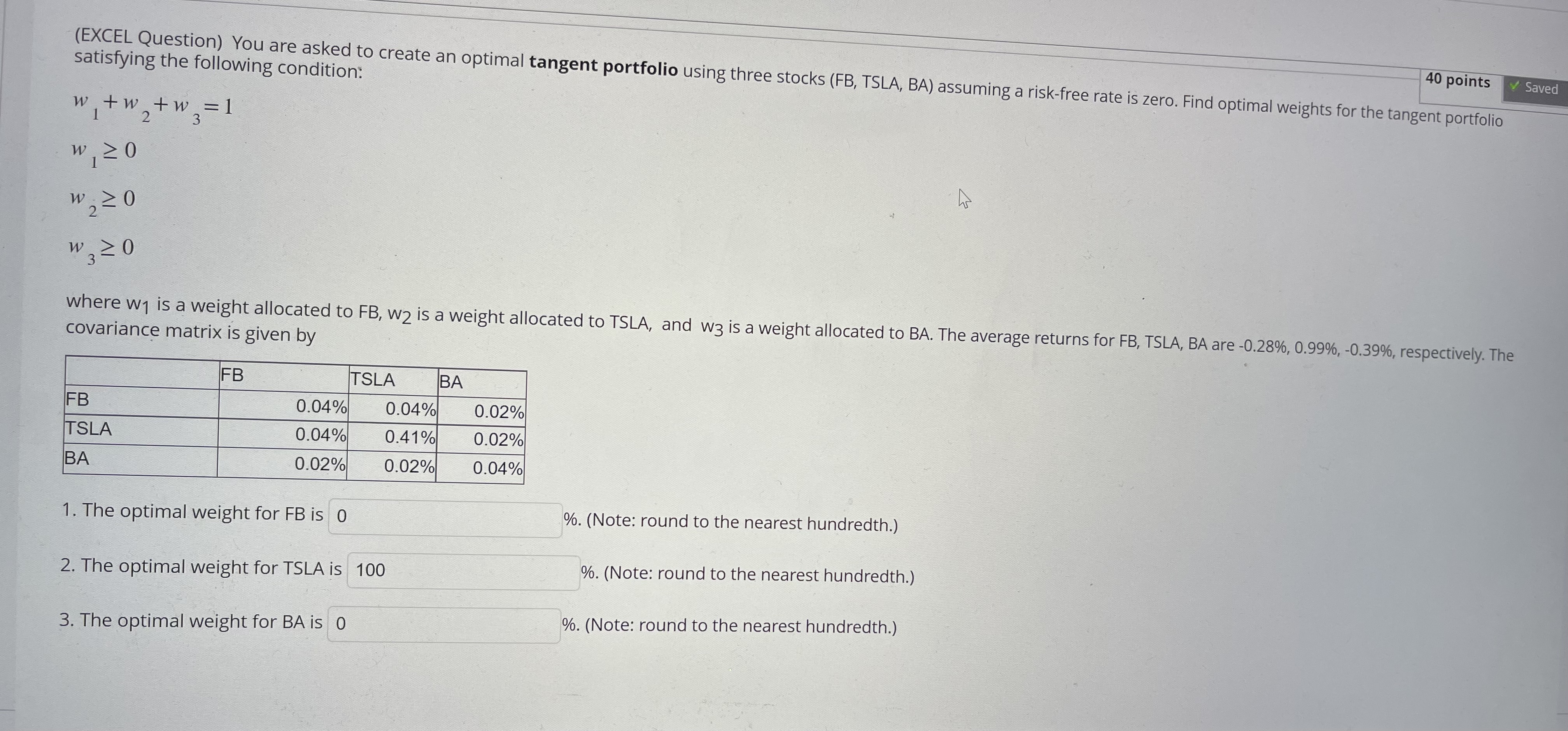

Question: 40 points Saved (EXCEL Question) You are asked to create an optimal tangent portfolio using three stocks (FB, TSLA, BA) assuming a risk-free rate is

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts