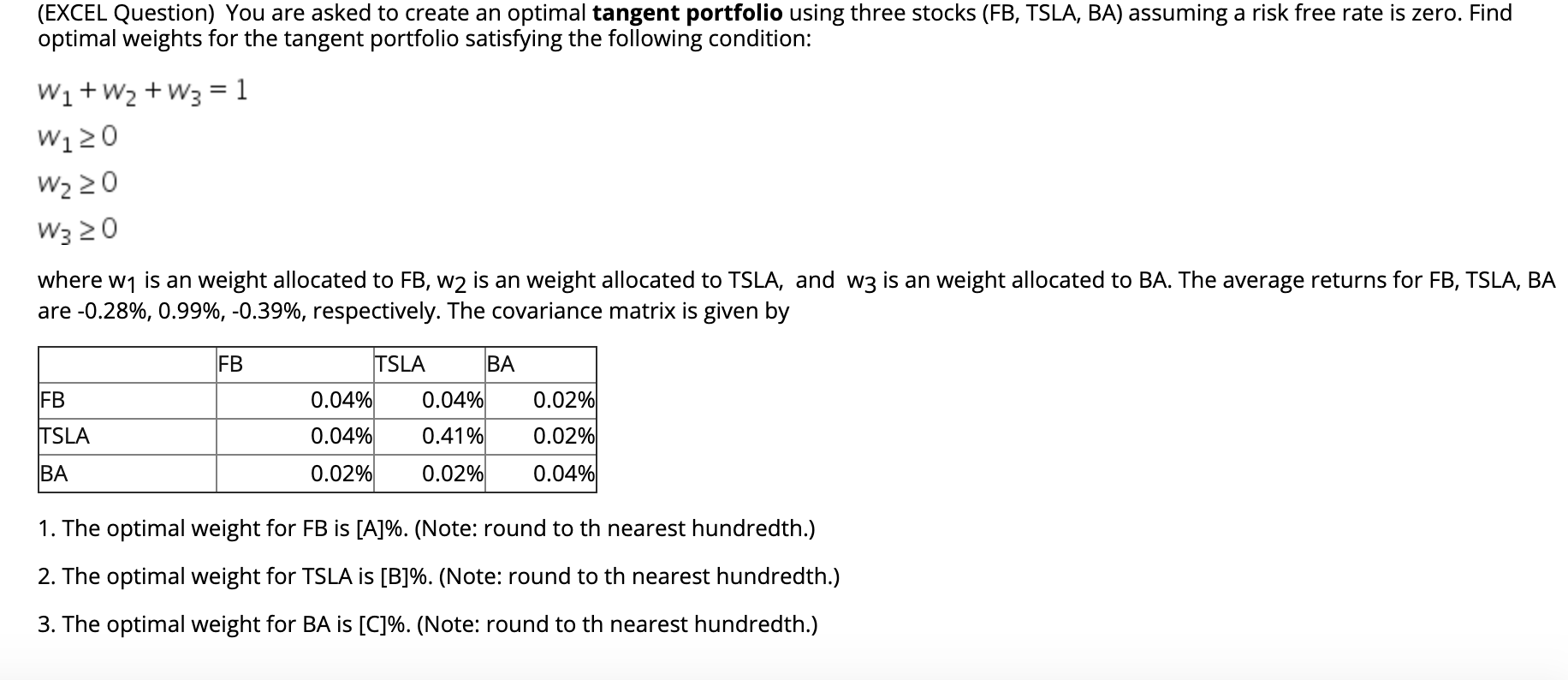

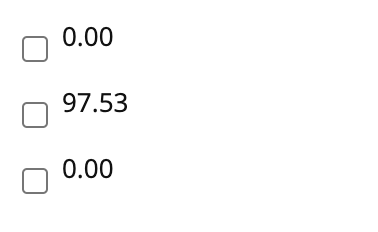

Question: (EXCEL Question) You are asked to create an optimal tangent portfolio using three stocks (FB, TSLA, BA) assuming a risk free rate is zero. Find

(EXCEL Question) You are asked to create an optimal tangent portfolio using three stocks (FB, TSLA, BA) assuming a risk free rate is zero. Find optimal weights for the tangent portfolio satisfying the following condition: Wi+W2+W3 = 1 W120 W220 W320 where W1 is an weight allocated to FB, W2 is an weight allocated to TSLA, and w3 is an weight allocated to BA. The average returns for FB, TSLA, BA are -0.28%, 0.99%, -0.39%, respectively. The covariance matrix is given by FB TSLA BA IFB 0.04% 0.04% 0.02% TSLA 0.04% 0.41% 0.02% BA 0.02% 0.02% 0.04% 1. The optimal weight for FB is [A]%. (Note: round to th nearest hundredth.) 2. The optimal weight for TSLA is [B]%. (Note: round to th nearest hundredth.) 3. The optimal weight for BA is [C]%. (Note: round to th nearest hundredth.) 0.00 97.53 0.00

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts