Question: 4:14 Files ...146 0 Part 2 (50 marks) Part two requires calculations to answer the questions. Furthermore, it requires qualitative explanations that convy your understanding

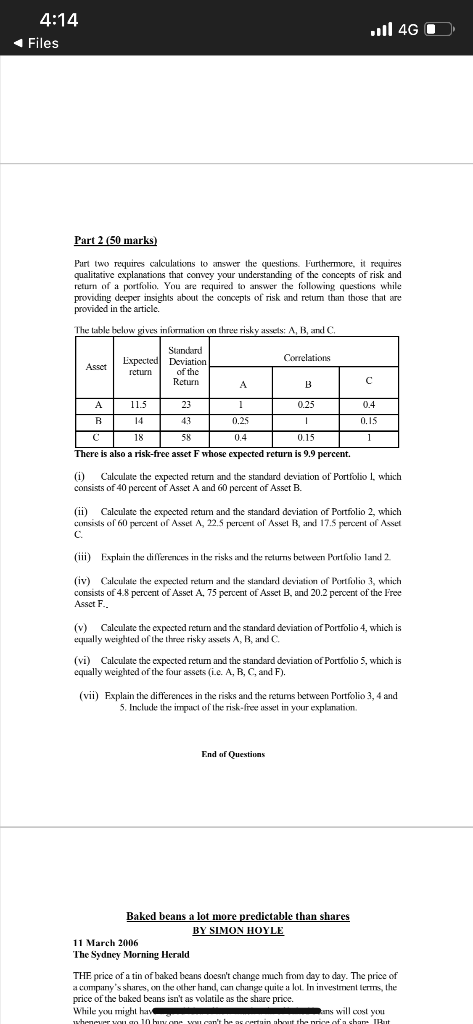

4:14 Files ...146 0 Part 2 (50 marks) Part two requires calculations to answer the questions. Furthermore, it requires qualitative explanations that convy your understanding of the concepts of risk and return of a portfolio. You are required to answer the following questions while providing deeper insights about the concepts of risk and retum than those that are provided in the article. The table below gives information on three risky assets: A, B, and C. Correlations Asset Expected return Standard Deviation of the Return A 11.5 1 .25 23 43 0 1 0.25 0 0.4 .15 1 18 0.4 0.15 There is also a risk-free asset F whose expected return is 9.9 percent. (i) Calculate the expected return and the standard deviation of Portfolio I, which consists of 40 percent of Asset A and 60 percent of Asset B. (ii) Calculate the expected retum and the standard deviation of Portfolio 2, which Censis of 60 percent of Asset A, 22.5 percent of Asset B, and 17.5 percent of Asset (iii) Explain the differences in the risks and the returns belween Portfolio and 2 (iv) Calculate the expected return and the standard deviation of Portfolio 3, which consists of 4.8 percent of Asset A, 75 percent of Asset B, and 20.2 percent of the Free Asset F.. (v) Calculate the expected return and the standard deviation of Portfolio 4, which is equally weighted of the three risky assets A, B, and C. (vi) Calculate the expected retum and the standard deviation of Portfolio 5, which is equally weighted of the four assets (i.e. A, B, C, and F). (vii) Explain the differences in the risks and the retums between Portfolio 3, 4 and 5. Include the impact of the risk-free asset in your explanation End of Questions Baked beans a lot more predictable than shares BY SIMON HOYLE 11 March 2006 The Sydney Morning Herald THE price of a tin of haked beans doesn't change much from day to day. The price of a company's shames, the other hand, can change quite a lot. In investment lets, the price of the baked beans isn't as volatile as the share price. While you might have ans will cost you when w 1 b one w can't bear the 113

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts