Question: 5. (16 pts) Consider a default-free bond that has three years to maturity, annual coupons of 4.65%, and is callable at par one year and

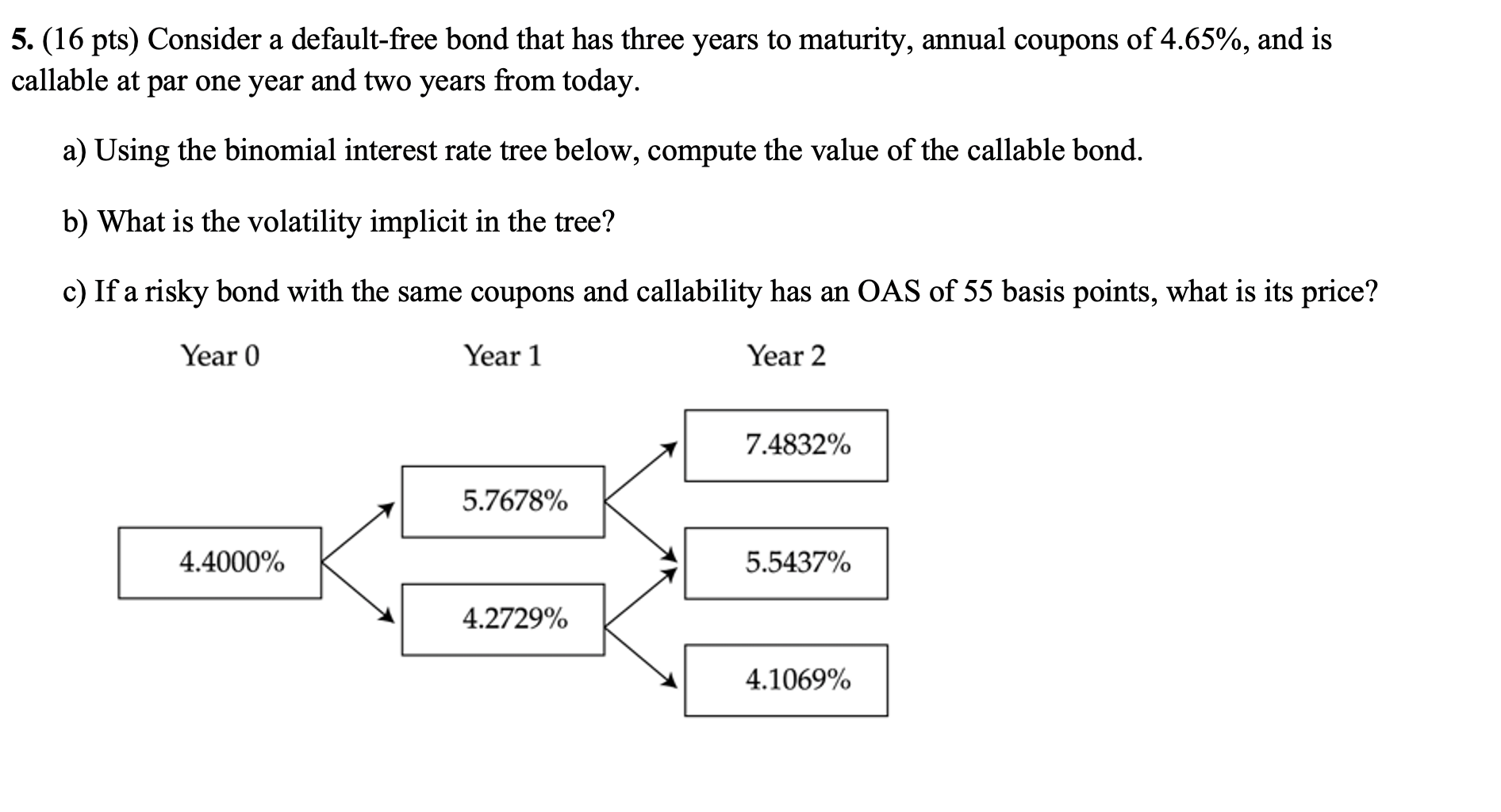

5. (16 pts) Consider a default-free bond that has three years to maturity, annual coupons of 4.65%, and is callable at par one year and two years from today. a) Using the binomial interest rate tree below, compute the value of the callable bond. > b) What is the volatility implicit in the tree? c) If a risky bond with the same coupons and callability has an OAS of 55 basis points, what is its price? Year 0 Year 1 Year 2 7.4832% 5.7678% 4.4000% 5.5437% 4.2729% 4.1069%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock