Question: 5. ( 7 points) (a) (5 points) Evaluate the appropriateness of the following CALM valuation expense assumptions for a life insurance block of business: A.

5. ( 7 points) (a) (5 points) Evaluate the appropriateness of the following CALM valuation expense assumptions for a life insurance block of business: A. The best estimate annual maintenance expense assumption is 60 per policy. This is based on the most recent expense study of the company. This includes expenses incurred to sell and underwrite policies, to perform the administration of the policies, and to pay claims. It does not include any overhead expenses or expenses associated with policyholder dividends. B. The maintenance expense inflation rate is 3% per year. C. Commissions and premium taxes are included separately in the valuation and are not subject to inflation. D. A margin for adverse deviation of 15% is applied to all expenses. E. Investment expenses for the assets supporting the liability are not included in the valuation. (b) (2 points) The company is implementing an initiative that is expected to reduce the annual maintenance expense by 5 per policy. Describe four considerations in updating the valuation expense assumption.

6. ( 11 points) (a) (4 points) Evaluate the following statements with respect to CALM valuation: A. The contract liability for a particular scenario is equal to the present value of the net liability cashflows discounted using risk free rates plus an appropriate margin. B. The contract liability for a block of business must be set to the maximum of the amount calculated under the prescribed scenarios. C. Each assumption is expressed in terms of a best estimate plus a margin for adverse deviation. D. The term of the liability is equal to the contractual term of the policy. (b) (1 point) List four considerations for setting an appropriate valuation investment strategy assumption. (c) (3 points) You are calculating CALM reserves for a life insurance portfolio that is backed solely by fixed income bonds. The company has decided to add a portfolio of diversified North American common shares to the fixed income assets. You have good historical data for these shares. (i) (2 points) Describe considerations for determining the valuation assumptions used for equity returns. (ii) (1 point) Describe changes to the investment strategy used in valuation due to the addition of equities.

2. (9 points) DEF, a Canadian Life Insurance Company, specializes in UL products. Recently, they decided to launch their first participating product, First Par. First Par is a whole life product with a guaranteed death benefit and annual cash dividends. (a) (3 points) DEF is planning the following dividend determination process for First Par: ? First Par dividends will be updated every three years in order to smooth experience over time. ? A single interest rate will be used for all First Par policyholders, regardless of issue date or other policyholder characteristics. ? Claims experience gains and losses from all products will be considered. Comment on how well the above dividend determination process reflects the contribution principle. (b) (6 points) You are given the following statements: A. Initial sales projections do not justify creating a separate participating account. Hence, there is no need for DEF to create a Par Account Management Policy. B. First Par will have several advantages over the existing UL products: ? DEF may claim qualifying par status, reducing LICAT required capital. ? DEF can hold lower PfADs on First Par compared to UL products. ? DEF will be able to realize a profit margin at 12% regardless of experience, as the full amount of any losses can be offset by reducing dividends. C. DEF will create a Dividend Policy, but it will not be disclosed publicly to reduce the risk of a lawsuit. D. The Appointed Actuary does not need to sign any additional opinions related to the dividends and the company's dividend policy, since there is no Par Account Management Policy. Evaluate the above statements

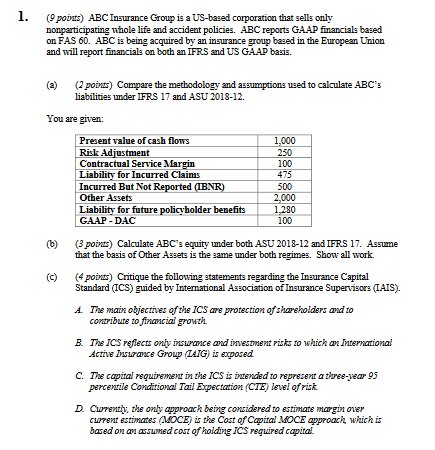

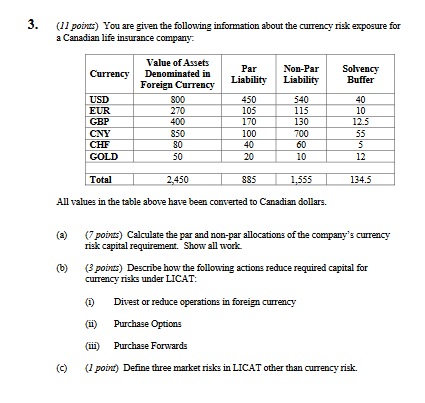

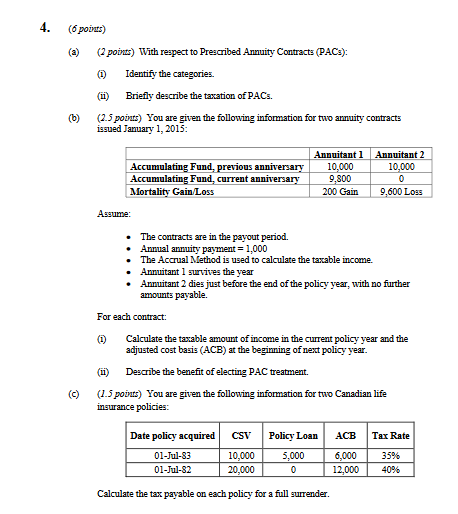

1. (9 point) ABC Insurance Group is a US-based corporation that sells only nonparticipating whole life and accident policies. ABC reports GAAP financials based on FAS 60. ABC is being acquired by an insurance group based in the European Union and will report financials on both an IFRS and US GAAP basis. (2) (2 points) Compare the methodology and assumptions used to calculate ABC's liabilities under IFRS 17 and ASU 2018-12. You are given: Present value of cash flows 1,000 Risk Adjustment 250 Contractual Service Margin 100 Liability for Incurred Claims 175 Incurred But Not Reported (IBNR) 500 Other Assets 2,000 Liability for future policyholder benefits 1,280 GAAP - DAC 100 (b) (3 points) Calculate ABC's equity under both ASU 2018-12 and IFRS 17. Assume that the basis of Other Assets is the same under both regimes. Show all work (9) (4 points) Critique the following statements regarding the Insurance Capital Standard (ICS) guided by International Association of Insurance Supervisors (IAIS). A. The main objectives of the 105 are protection of shareholders and to contribute to financial growth B. The ICS reflects only insurance and investment risks to which an International Active Inname Group (IAIG) is exposed C. The capital requirement in the IC5 is intended to represent a three-year 95 percentile Conditional Tail Expectation (CTE) level ofrisk D. Currently the only approach being considered to estimate margin over current estimates (MOCE) is the Cost of Capital MOCE approach which is based on an assured cost of holding ICS required capital3. (II points) You are given the following information about the currency risk exposure for a Canadian life insurance company. Value of Assets Currency Denominated in Par Non-Par Solvency Foreign Currency Liability Liability Buffer USD 30 0 450 540 40 EUR 270 105 115 10 GBP 400 170 130 12.5 CNY 850 100 700 55 CHF 80 40 60 5 GOLD 50 20 10 12 Total 2,450 885 1.555 134.5 All value: in the table above have been converted to Canadian dollars. (7 points) Calculate the par and non-par allocations of the company's currency risk capital requirement. Show all work (bj (3 points) Describe how the following actions reduce required capital for currency risks under LICAT: (D) Divest or reduce operations in foreign currency (mi) Purchase Options (mii) Purchase Forwards () (/ point) Define three market risks in LICAT other than currency risk.4. (6 points) () (7 point) With respect to Prescribed Annuity Contracts (PACE): Identify the categories. (m) Briefly describe the taxation of PACs. (bj (25 points) You are given the following information for two annuity contracts issued January 1, 2015: Annuitant 1 Annuitant 2 Accumulating Fund, previous anniversary 10,000 10,000 Accumulating Fund, current anniversary 9.800 0 Mortality Cain Loss 200 Gain 9.600 Love Asgume: The contracts are in the payout period. Annual annuity payment = 1,000 The Accrual Method is used to calculate the taxable income. Annuitant 1 survives the year Annuitant 2 dies just before the end of the policy year, with no further amounts payable. For each contract: (D) Calculate the taxable amount of income in the current policy year and the adjusted cost basis (ACB) at the beginning of next policy year. (mi) Describe the benefit of electing PAC treatment. (1.5 pounds) You are given the following information for two Canadian life insurance policies: Date policy acquired CSV Policy Loan ACB Tax Rate 01-Jul-83 10,000 5.000 6,000 01-Jul-82 20,000 0 12,000 40% Calculate the tax payable on each policy for a full surrender

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts