Question: 5. Given the ABS & ABS CDO shown below , what is the minimum loss on the portfolio of underlying assets when: assets a. Lower

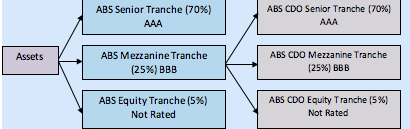

5. Given the ABS & ABS CDO shown below , what is the minimum loss on the portfolio of underlying assets when:

assets

a. Lower two ABS tranches have a 100% loss of principal?

b. Senior ABS tranche a 50% has loss of principal?

c. Equity ABS CDO tranche has a 100% loss of principal?

d. Mezzanine ABS CDO tranche has a 100% loss of principal?

e. Senior ABS CDO tranche has a 50% loss of principal?

f. Senior ABS CDO tranche has a 100% loss of principal?

g. Why is it likely that the AAA-rated tranche of this ABS CDO is more risky than the AAA-rated tranche of the ABS?

h. Why are the risks in ABS CDOs misjudged by the market? What did we learn about this in 2007?

ABS Senior Tranche (70%) AAA ABS CDO Senior Tranche (70%) AAA Assets ABS Mezzanine Tranche (25%) BBB ABS CDO Mezzanine Tranche (25%) BBB ABS Equity Tranche (5%) Not Rated ABS CDO Equity Tranche (5%) Not Rated ABS Senior Tranche (70%) AAA ABS CDO Senior Tranche (70%) AAA Assets ABS Mezzanine Tranche (25%) BBB ABS CDO Mezzanine Tranche (25%) BBB ABS Equity Tranche (5%) Not Rated ABS CDO Equity Tranche (5%) Not Rated

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts