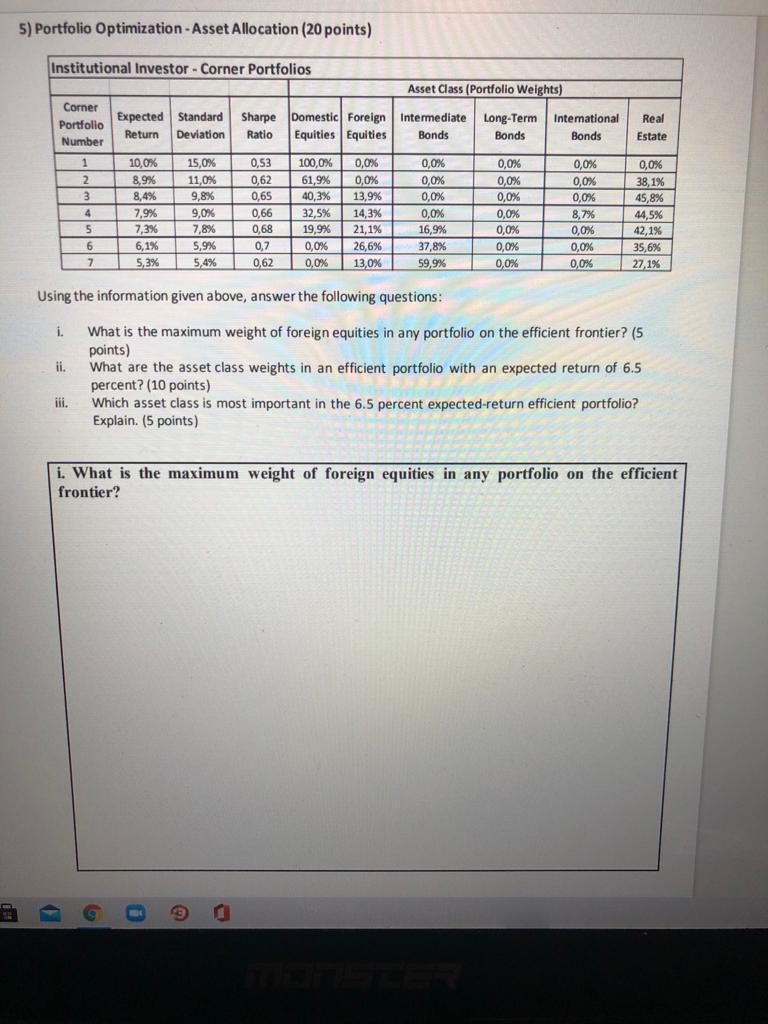

Question: 5) Portfolio Optimization - Asset Allocation (20 points) Institutional Investor - Corner Portfolios Asset Class (Portfolio Weights) Corner Portfolio Number Expected Standard Sharpe Domestic Foreign

5) Portfolio Optimization - Asset Allocation (20 points) Institutional Investor - Corner Portfolios Asset Class (Portfolio Weights) Corner Portfolio Number Expected Standard Sharpe Domestic Foreign Intermediate Return Deviation Ratio Equities Equities Bonds Long-Term Bonds Intemational Bonds Real Estate 1 0.53 2 3 4 5 6 7 10,0% 8.9% 8,4% 7,9% 7,3% 6,1% 5,3% 15,0% 11,0% 9,8% 9,0% 7,8% 5,9% 5,4% 0,62 0,65 0,66 0,68 0,7 100,0% 61,9% 40,3% 32.5% 19,9% 0,0% 0,0% 0,0% 0,0% 13.9% 14,3% 21,1% 26,6% 13,0% 0,0% 0,0% 0,0% 0,0% 16,9% 37,8% 59,9% 0,0% 0,0% 0,0% 0,0% 0,0% 0,0% 0,0% 0,0% 0,0% 0,0% 8,7% 0,0% 0,0% 0,0% 0,0% 38,1% 45,8% 44,5% 42,1% 35,6% 27,1% 0,62 Using the information given above, answer the following questions: i. ii. What is the maximum weight of foreign equities in any portfolio on the efficient frontier? (5 points) What are the asset class weights in an efficient portfolio with an expected return of 6.5 percent? (10 points) Which asset class is most important in the 6.5 percent expected-return efficient portfolio? Explain. (5 points) i. What is the maximum weight of foreign equities in any portfolio on the efficient frontier? G

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts