Question: 6.2- Based on the information in problem 6.1, draw the payoff profile for a long krone put option at expiration. Note that these exchange rates

6.2- Based on the information in problem 6.1, draw the payoff profile for a long krone put option at expiration. Note that these exchange rates reciprocals of those in Problem 6.1

/DKK spot exchange rate STDKK at expiration

0.12500 0.11905 0.11876 0.11848 0.11820 0.11792

Put Value

Label your axes and plot each point. Draw a profit/loss graph for this long krone put at expiration. Refer to the long put in Exhibit 6.4 for reference

Here is the problem 6.1

6.4

Construct an option position (i.e., some combination of calls and/or puts) with the same risk profile ( Call$/A$ versus S$/A$) as a forward contract to buy A$ at a forward price of F1$/A$=$0.75/A$. Use both words and graphs.

a) Label the axes

b) Identify the asset underlying the options.

c) Indicate whether each option is a put or a call.

d) Indicate whether youre buying or selling the option.

e) Indicate the exercise price.

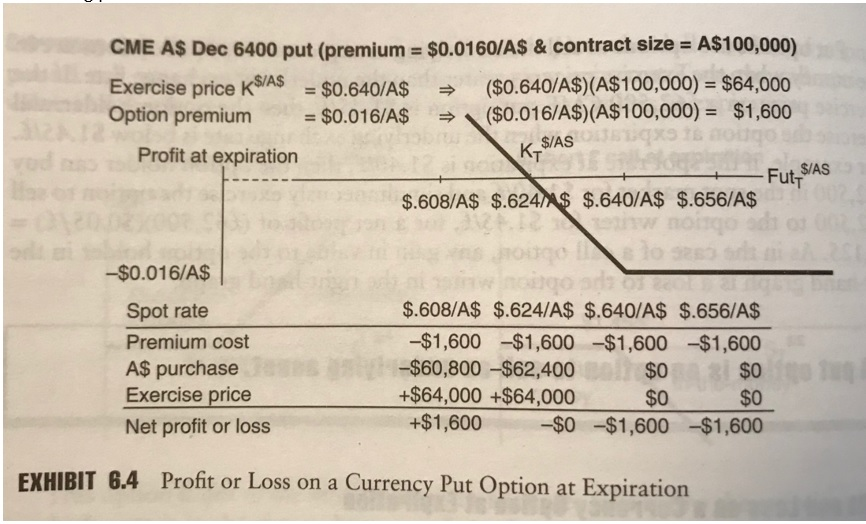

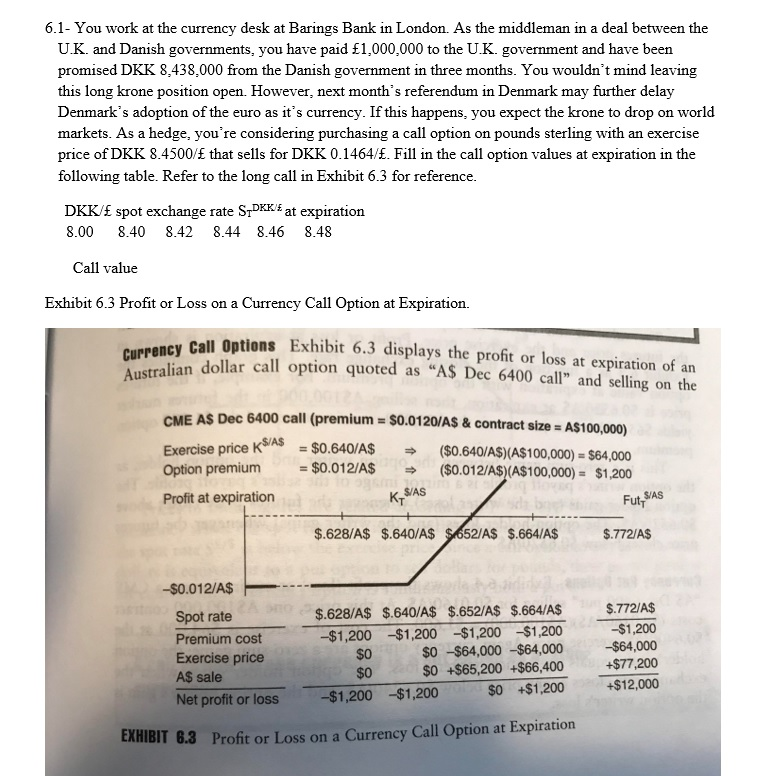

CME A$ Dec 6400 put (premium = $0.0160/A$ & contract size = A$100,000) Exercise price K$/A$ = $0.640/A$ ($0.640/A$)(A$100,000) = $64,000 Option premium = $0.016/A$ ($0.016/A$)(A$100,000) = $1,600 $/AS Profit at expiration K_$/AS - Fut S/AS $.608/A$ $.6241 $ $.640/A$ $.656/A$ -$0.016/A$ Spot rate Premium cost A$ purchase Exercise price Net profit or loss $.608/A$ $.624/A$ $.640/A$ $.656/A$ -$1,600 $1,600 $1,600 $1,600 -$60,800 -$62,400 $0 $0 +$64,000 +$ 64,000 $0 $0 +$1,600 $0 $1,600 $1,600 EXHIBIT 6.4 Profit or Loss on a Currency Put Option at Expiration 6.1. You work at the currency desk at Barings Bank in London. As the middleman in a deal between the U.K. and Danish governments, you have paid 1,000,000 to the U.K. government and have been promised DKK 8,438.000 from the Danish government in three months. You wouldn't mind leaving this long krone position open. However, next month's referendum in Denmark may further delay Denmark's adoption of the euro as it's currency. If this happens, you expect the krone to drop on world markets. As a hedge, you're considering purchasing a call option on pounds sterling with an exercise price of DKK 8.4500/ that sells for DKK 0.1464/. Fill in the call option values at expiration in the following table. Refer to the long call in Exhibit 6.3 for reference. DKK/ spot exchange rate SDKK/E at expiration 8.00 8.40 8.42 8.44 8.46 8.48 Call value Exhibit 6.3 Profit or Loss on a Currency Call Option at Expiration. y Call Options Exhibit 6.3 displays the profit or loss at expiration of an in dollar call option quoted as "A$ Dec 6400 call" and selling on the Australian dollar call on CME AS Dec 6400 call (premium = $0.0120/AS & contract size = A$100.000) Exercise price K = $0.640/A$ ($0.640/A$)(A$100,000) = $64,000 Option premium = $0.012/A$ ($0.012/A$)(A$100,000) = $1.200 Profit at expiration K, S/AS Fut S/AS $.628/A$ $.640/A$ $1652/A$ $.664/A$ $.772/A$ -$0.012/A$ Spot rate Premium cost Exercise price A$ sale Net profit or loss $.628/A$ $.640/A$ $.652/A$ $.664/A$ -$1,200 $1,200 $1,200 $1,200 $0 $0-$64,000 $64,000 $0 $0+$65,200 $66,400 -$1,200 $1,200 $0 $1,200 $.772/A$ -$1,200 -$64,000 +$77,200 +$12,000 CAMIBIT 8.3 Profit or Loss on a Currency Call Option at Expiration

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts