Question: 7. Functional form misspecification and RESET Consider the following model that satisfies assumption MLR.4: y = Bo + B1X1 + ... + Bxxx + u

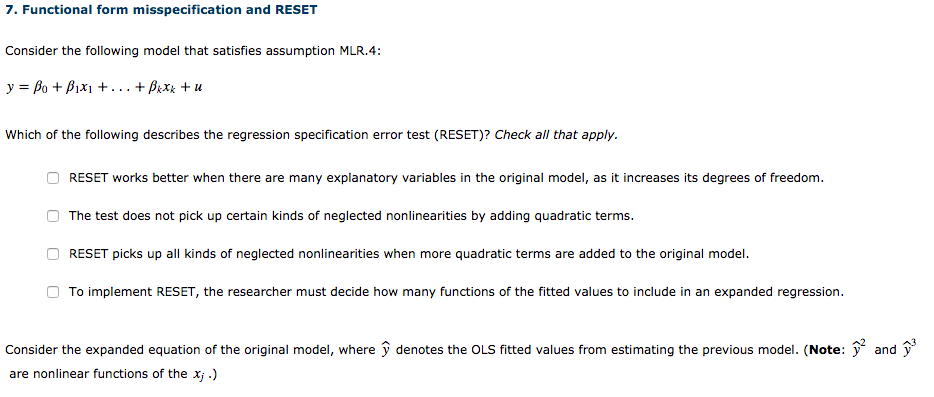

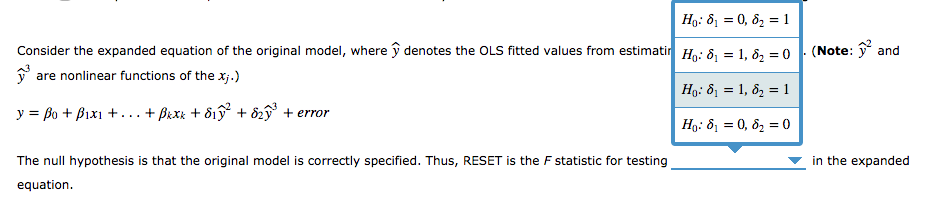

7. Functional form misspecification and RESET Consider the following model that satisfies assumption MLR.4: y = Bo + B1X1 + ... + Bxxx + u Which of the following describes the regression specification error test (RESET)? Check all that apply. RESET works better when there are many explanatory variables in the original model, as it increases its degrees of freedom. The test does not pick up certain kinds of neglected nonlinearities by adding quadratic terms. RESET picks up all kinds of neglected nonlinearities when more quadratic terms are added to the original model. To implement RESET, the researcher must decide how many functions of the fitted values to include in an expanded regression. Consider the expanded equation of the original model, where y denotes the OLS fitted values from estimating the previous model. (Note: 12 and y are nonlinear functions of the xj.) H:8, = 0, 82 = 1 Consider the expanded equation of the original model, where denotes the OLS fitted values from estimatir Ho: 81 = 1, 8z = 0 (Note: 2 and O are nonlinear functions of the xj.) H: 8 = 1, 82 = 1 y = po + Bx + ... + Bxxx + 8192 + 829 + error H: 8 = 0, 82 = 0 in the expanded The null hypothesis is that the original model is correctly specified. Thus, RESET is the F statistic for testing equation. 7. Functional form misspecification and RESET Consider the following model that satisfies assumption MLR.4: y = Bo + B1X1 + ... + Bxxx + u Which of the following describes the regression specification error test (RESET)? Check all that apply. RESET works better when there are many explanatory variables in the original model, as it increases its degrees of freedom. The test does not pick up certain kinds of neglected nonlinearities by adding quadratic terms. RESET picks up all kinds of neglected nonlinearities when more quadratic terms are added to the original model. To implement RESET, the researcher must decide how many functions of the fitted values to include in an expanded regression. Consider the expanded equation of the original model, where y denotes the OLS fitted values from estimating the previous model. (Note: 12 and y are nonlinear functions of the xj.) H:8, = 0, 82 = 1 Consider the expanded equation of the original model, where denotes the OLS fitted values from estimatir Ho: 81 = 1, 8z = 0 (Note: 2 and O are nonlinear functions of the xj.) H: 8 = 1, 82 = 1 y = po + Bx + ... + Bxxx + 8192 + 829 + error H: 8 = 0, 82 = 0 in the expanded The null hypothesis is that the original model is correctly specified. Thus, RESET is the F statistic for testing equation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts