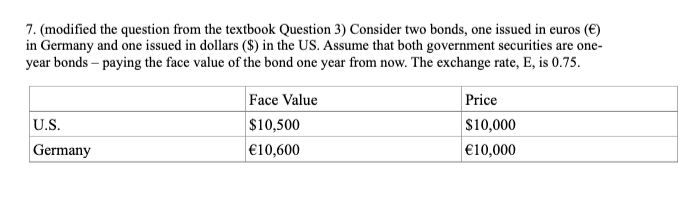

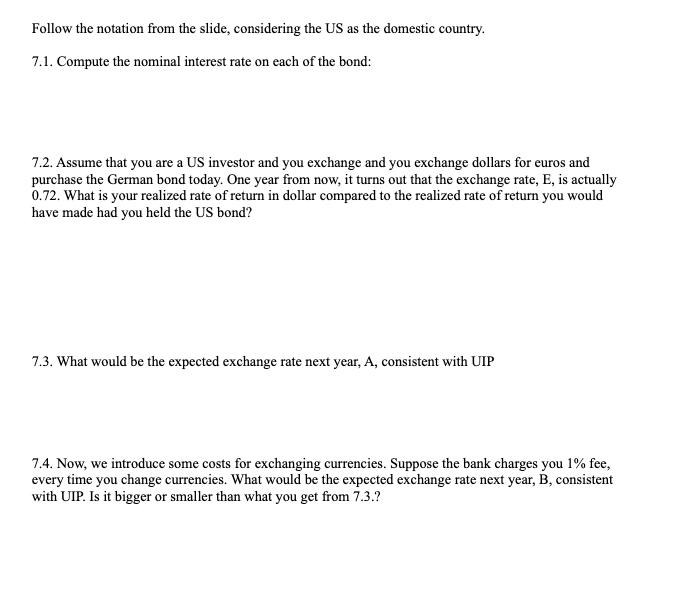

Question: 7. (modified the question from the textbook Question 3) Consider two bonds, one issued in euros (() in Germany and one issued in dollars ($)

7. (modified the question from the textbook Question 3) Consider two bonds, one issued in euros (() in Germany and one issued in dollars ($) in the US. Assume that both government securities are one- year bonds - paying the face value of the bond one year from now. The exchange rate, E, is 0.75. Face Value Price U.S. $10,500 $10,000 Germany (10,600 E10,000Follow the notation from the slide, considering the US as the domestic country. 7.1. Compute the nominal interest rate on each of the bond: 7.2. Assume that you are a US investor and you exchange and you exchange dollars for euros and purchase the German bond today. One year from now, it turns out that the exchange rate, E, is actually 0.72. What is your realized rate of return in dollar compared to the realized rate of return you would have made had you held the US bond? 7.3. What would be the expected exchange rate next year, A, consistent with UIP 7.4. Now, we introduce some costs for exchanging currencies. Suppose the bank charges you 1% fee, every time you change currencies. What would be the expected exchange rate next year, B, consistent with UIP. Is it bigger or smaller than what you get from 7.3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts