Question: 8. In this exercise you need to describe an immunization strategy for a portfolio, given the factors in Table 4.3. The term structures of interest

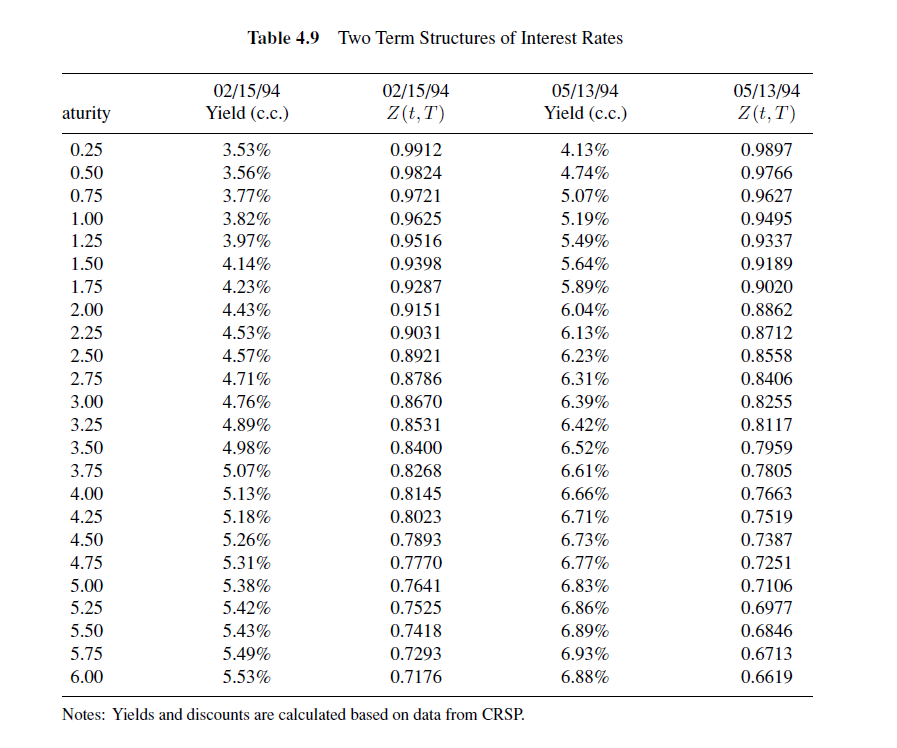

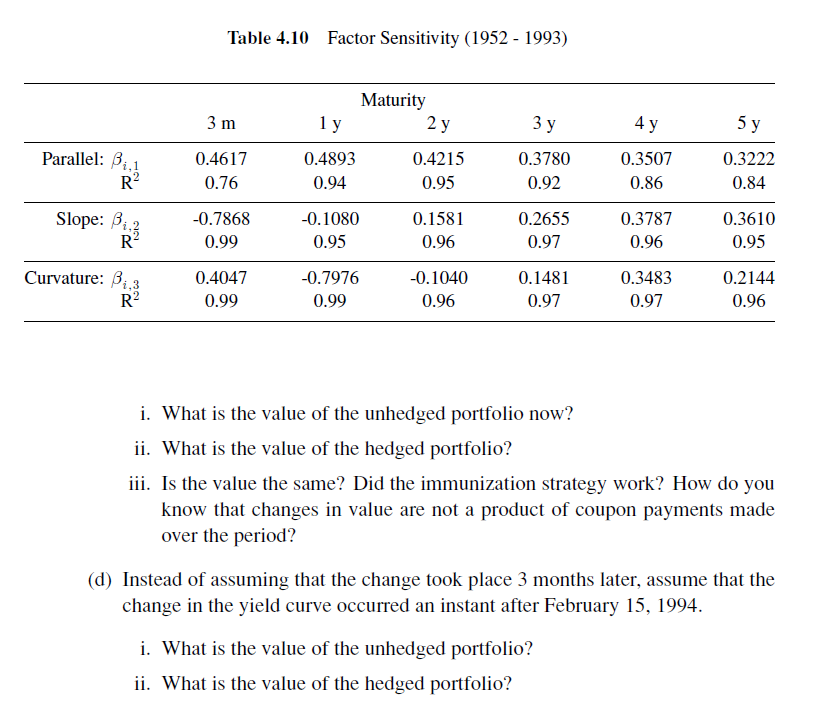

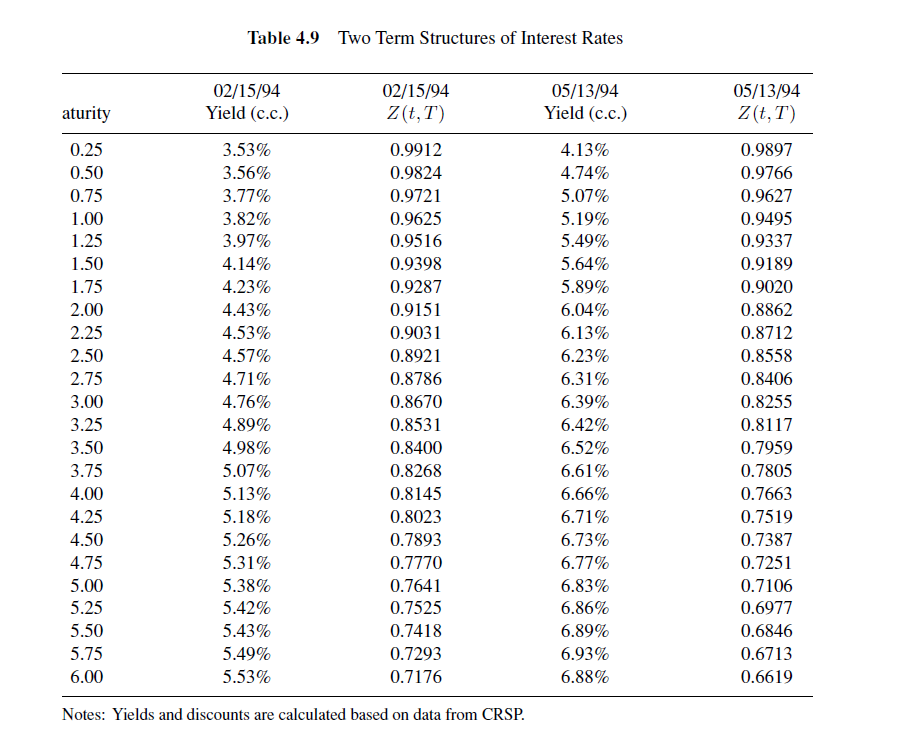

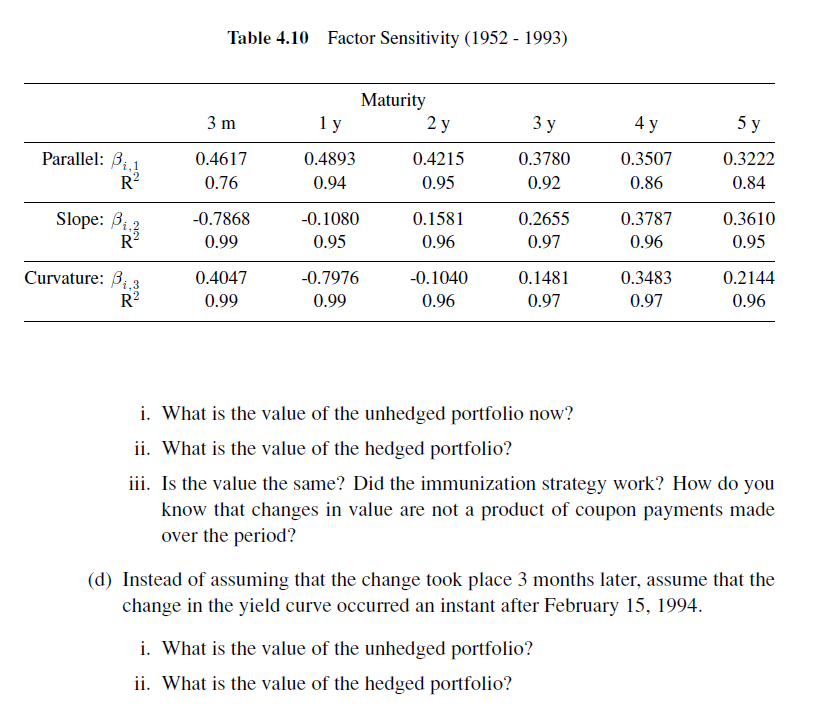

8. In this exercise you need to describe an immunization strategy for a portfolio, given the factors in Table 4.3. The term structures of interest rates at two dates are in Table 4.9. (a) You are standing at February 15. 1994 (see table) and you hold the following portfolio: a Long $30 million of a 6year inverse floater with coupon paid quarterly a Long $30 million of a 4year oating rate bond with a 45 basis point spread paid semiannually I Short $20 million of a 3year coupon bond paying 4% semiannually i. What is the total value of the portfolio? ii. Compute the dollar duration of the portfolio. (b) You are worried about interest rate volatility. You decided to hedge your portfolio with the following bonds: o A 3month zero coupon bond a A 6year zero coupon bond i. How much should you go shortflong on these bonds in order to make the portfolio immune to interest rate changes? ii. What is the total value of the portfolio now? (c) Assume that it is now May 13, 1994 and that the yield curve has changed accordingly. Table 4.9 Two Term Structures of Interest Rates 02/15/94 02/15/94 05/13/94 05/13/94 aturity Yield (c.c.) Z (t, T) Yield (c.c.) Z (t, T) 0.25 3.53% 0.9912 4.13% 0.9897 0.50 3.56% 0.9824 4.74% 0.9766 0.75 3.77% 0.9721 5.07% 0.9627 1.00 3.82% 0.9625 5.19% 0.9495 1.25 3.97% 0.9516 5.49% 0.9337 1.50 4.14% 0.9398 5.64% 0.9189 1.75 4.23% 0.9287 5.89% 0.9020 2.00 4.43% 0.9151 6.04% 0.8862 2.25 4.53% 0.9031 6.13% 0.8712 2.50 4.57% 0.8921 6.23% 0.8558 2.75 4.71% 0.8786 6.31% 0.8406 3.00 4.76% 0.8670 6.39% 0.8255 3.25 4.89% 0.8531 6.42% 0.8117 3.50 4.98% 0.8400 6.52% 0.7959 3.75 5.07% 0.8268 6.61% 0.7805 4.00 5.13% 0.8145 6.66% 0.7663 4.25 5.18% 0.8023 6.71% 0.7519 4.50 5.26% 0.7893 6.73% 0.7387 4.75 5.31% 0.7770 6.77% 0.7251 5.00 5.38% 0.7641 6.83% 0.7106 5.25 5.42% 0.7525 6.86% 0.6977 5.50 5.43% 0.7418 6.89% 0.6846 5.75 5.49% 0.7293 6.93% 0.6713 6.00 5.53% 0.7176 6.88% 0.6619 Notes: Yields and discounts are calculated based on data from CRSP.Table 4.11] Factor Sensitivity (1952 1993) Maturity 3 m 1 y '2 y 3 y 4 y 5 y Parallel: 137.1 0.4317 0.4393 0.4215 0.3730 0.3507 0.3222 R2 0.75 0.94 0.95 0.92 0.315 0.34 Slope: 171.2 47.7363 0.1030 0.1531 0.2355 0.3737 0.3510 132 0.99 0.95 0.915 0.97 0.95 0.95 Curvature: 171.3 0.4047 0.7973 0.1040 0.1431 0.3433 0.2144 R2 0.99 0.99 0.95 0.97 0.97 0.96 i. What is the value of the unhedged portfolio now? ii. What is the value of the hedged portfolio? iii. Is the value the same? Did the immunization strategy work? How do you know that changes in value are not a product of coupon payments made over the period? ((1) Instead of assuming that the change took place 3 months later, assume that the change in the yield curve occurred an instant after February 15, 1994. i. What is the value of the unhedged portfolio? ii. What is the value of the hedged portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts