Question: A borrower has a three-year, interest-only floating rate loan with a notional principal amount of $100,000 from a lender. The current term structure has 1=0.08,

A borrower has a three-year, interest-only floating rate loan with a notional principal amount of $100,000 from a lender. The current term structure has 1=0.08, 2=0.09and 3=0.095. It was established that the swap rate = 0.0942. Suppose that one year after the swap is arranged, the term structure of interest rates is as follows:

(a) Determine the market value of the swap to the payer (b) Suppose that a new two-year swap is arranged at time 1. Determine the swap rate for this new swap

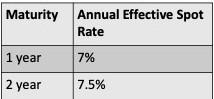

Maturity Annual Effective Spot Rate 1 year 7% 2 year 7.5% Maturity Annual Effective Spot Rate 1 year 7% 2 year 7.5%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock