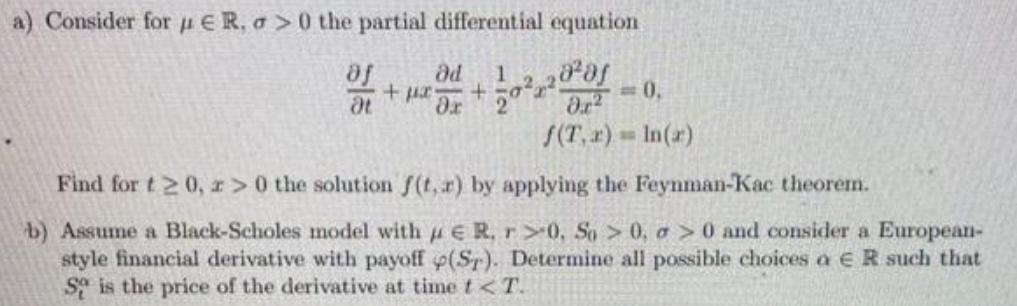

Question: a) Consider for ER, a>0 the partial differential equation ad 1 + 2 + of at ,22 -0. 8.2 f(T.x)= In(a) Find for t

a) Consider for ER, a>0 the partial differential equation ad 1 + 2 + of at ,22 -0. 8.2 f(T.x)= In(a) Find for t 0, z>0 the solution f(t,r) by applying the Feynman-Kac theorem. b) Assume a Black-Scholes model with ER, r>0, So > 0, a>0 and consider a European- style financial derivative with payoff p(Sr). Determine all possible choices a ER such that So is the price of the derivative at time t < T.

Step by Step Solution

★★★★★

3.31 Rating (154 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

3 xy2y 5xy This can be written as x dx 2y 5xy on sie rearranging we get 22 24 5 ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock