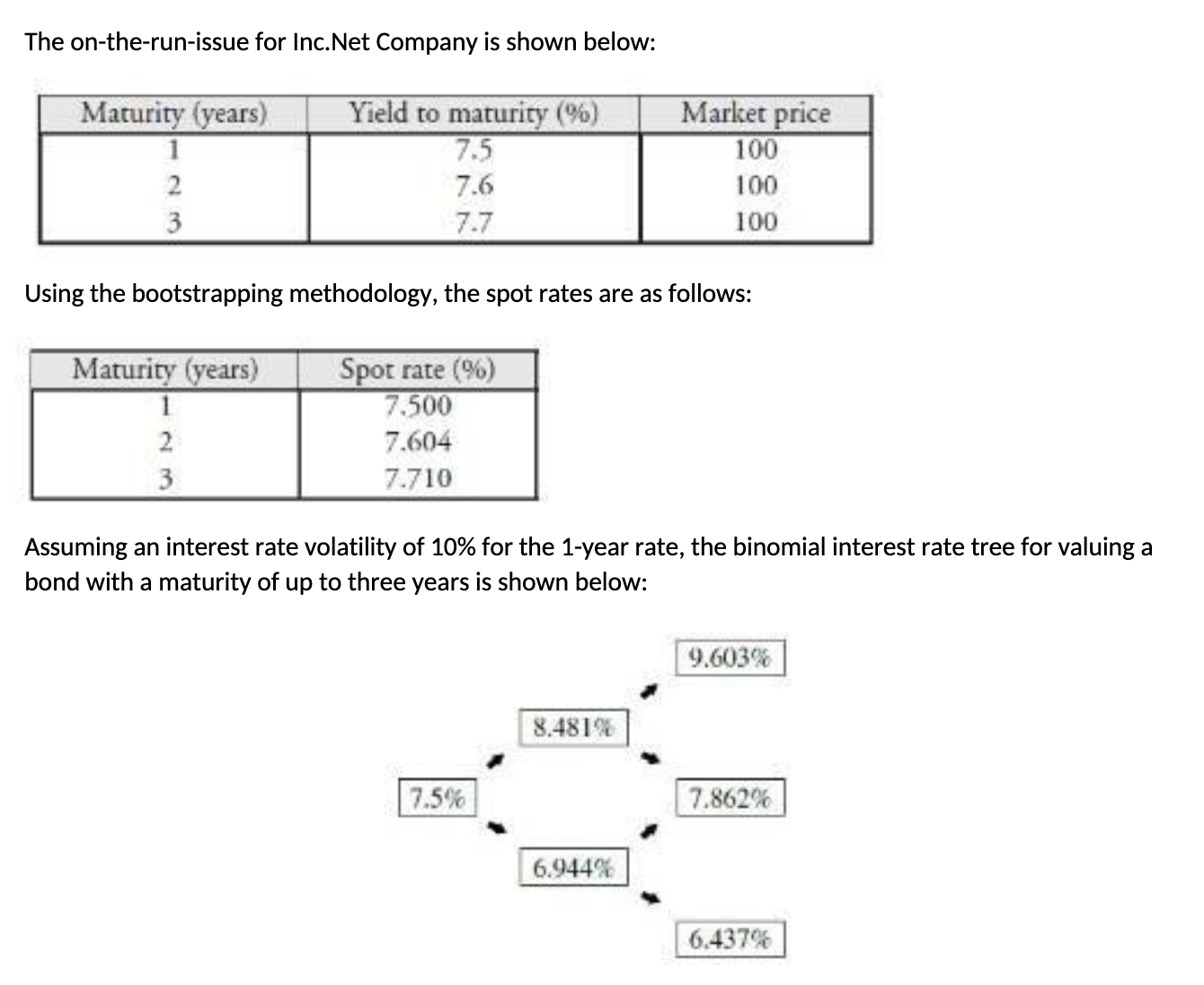

Question: a. Demonstrate using the 2-year on-the-run issue that the binomial interest rate tree above is in fact an arbitrage-free tree. b. Demonstrate using the 3-year

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts