Question: a. Explain the Global Minimum variance Portfolio. b. Why should an investor invest in a portfolio in the efficient frontier? c. Consider the following scenario

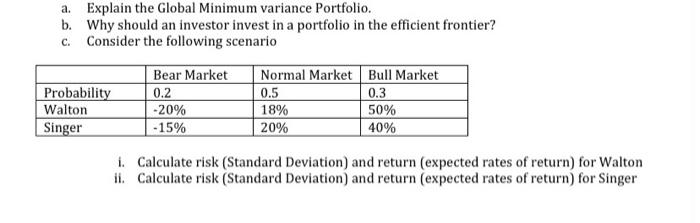

a. Explain the Global Minimum variance Portfolio. b. Why should an investor invest in a portfolio in the efficient frontier? c. Consider the following scenario Normal Market Bull Market 0.5 0.3 Probability Walton Singer Bear Market 0.2 -20% -15% 18% 20% 50% 40% 1. Calculate risk (Standard Deviation) and return (expected rates of return) for Walton ii. Calculate risk (Standard Deviation) and return (expected rates of return) for Singer

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock