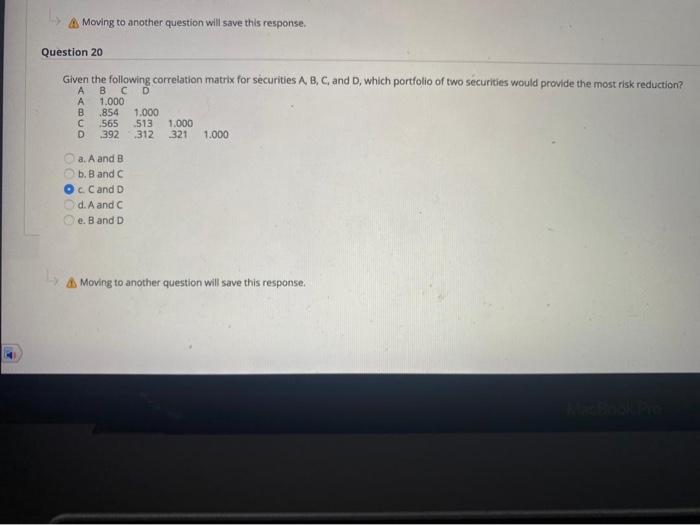

Question: A Moving to another question will save this response. Question 20 Given the following correlation matrix for securities A, B, C, and D, which portfolio

A Moving to another question will save this response. Question 20 Given the following correlation matrix for securities A, B, C, and D, which portfolio of two securities would provide the most risk reduction? 1.000 B 854 1.000 565 513 1.000 D .392 .312 321 1.000 . a. A and B b. B and C c. Cand D d. A and C e. Band D Moving to another question will save this response

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock