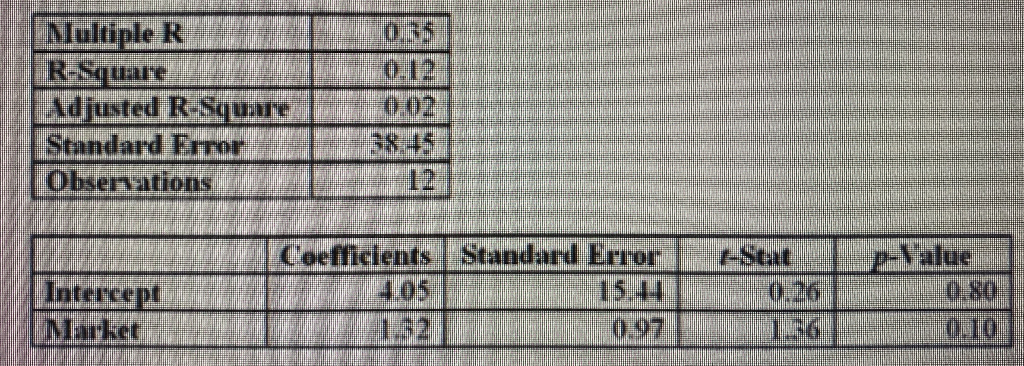

Question: (a) _______ % of the variance is explained by this regression. (b) The firm-specific risk is ______. (c) The beta of this stock is ______.

(a) _______ % of the variance is explained by this regression.

(b) The firm-specific risk is ______.

(c) The beta of this stock is ______. Hence, the stock is ______% riskier than the market.

(d) The characteristic line for this stock is E(Rstock) = ___ + ___ E(Rmarket)

(e) The alpha(intercept) has a t-Stat = ______. This is ______ than 2. Therefore, we can treat this alpha as if its equalot equal to (circle one) zero and conclude the CAPM is valid/invalid (circle one) for this stock.

Multiple R | R-Square | Adjusted R-S | Standard Error | Observations p-Value Intercept Market Coefficients | Standard Error 15.14 0.97 0.80 182 0.26 136

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts