Question: A portfolio is to be constructed from two stocks whose mean and variance of return rates are given below Stock Mean return rate Variance of

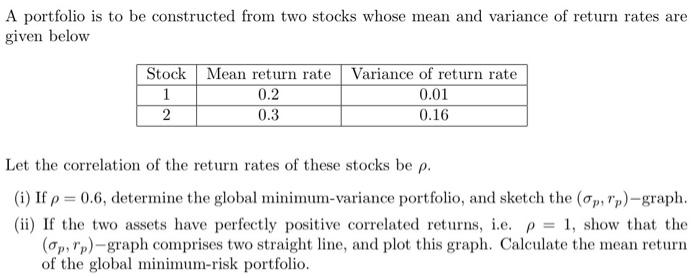

A portfolio is to be constructed from two stocks whose mean and variance of return rates are given below Stock Mean return rate Variance of return rate 1 0.2 0.3 0.01 0.16 2 Let the correlation of the return rates of these stocks be p. (i) If p = 0.6, determine the global minimum-variance portfolio, and sketch the (op, rp)-graph. (ii) If the two assets have perfectly positive correlated returns, i.e. p = 1, show that the (op, Tp)-graph comprises two straight line, and plot this graph. Calculate the mean return of the global minimum-risk portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock