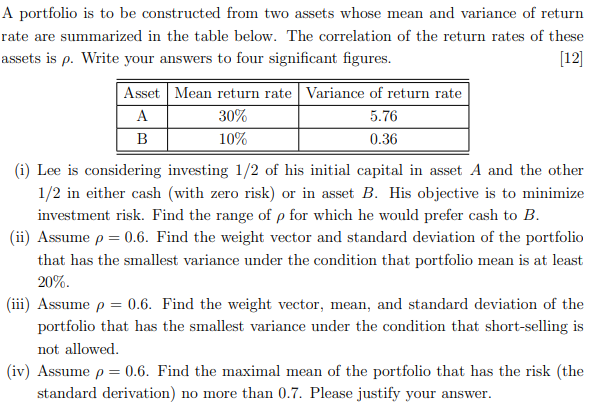

Question: A portfolio is to be constructed from two assets whose mean and variance of return rate are summarized in the table below. The correlation of

A portfolio is to be constructed from two assets whose mean and variance of return rate are summarized in the table below. The correlation of the return rates of these assets is . Write your answers to four significant figures. [12] (i) Lee is considering investing 1/2 of his initial capital in asset A and the other 1/2 in either cash (with zero risk) or in asset B. His objective is to minimize investment risk. Find the range of for which he would prefer cash to B. (ii) Assume =0.6. Find the weight vector and standard deviation of the portfolio that has the smallest variance under the condition that portfolio mean is at least 20%. (iii) Assume =0.6. Find the weight vector, mean, and standard deviation of the portfolio that has the smallest variance under the condition that short-selling is not allowed. (iv) Assume =0.6. Find the maximal mean of the portfolio that has the risk (the standard derivation) no more than 0.7. Please justify your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts