Question: (a) Shown below is a binomial tree for a 6% counon bond based on an interest rate volatil (b) Suppose the bond above is putable

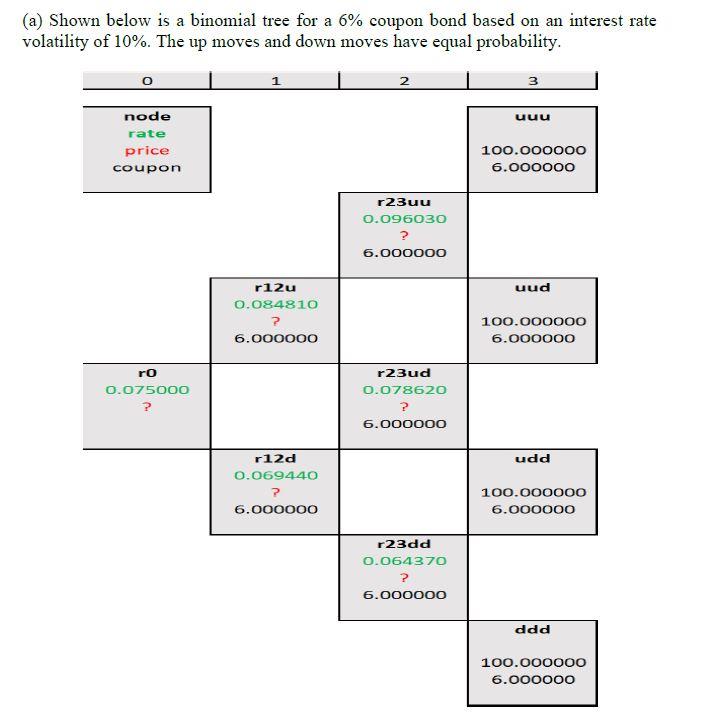

(a) Shown below is a binomial tree for a 6% counon bond based on an interest rate volatil (b) Suppose the bond above is putable at par from Year 1. Compute the value of the bond at time 0 . (a) Shown below is a binomial tree for a 6% counon bond based on an interest rate volatil (b) Suppose the bond above is putable at par from Year 1. Compute the value of the bond at time 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock