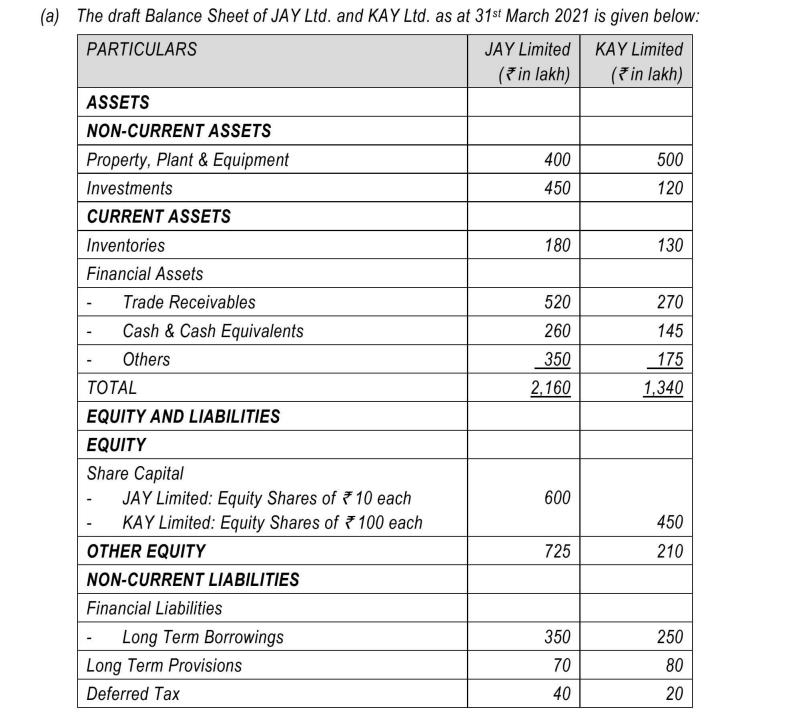

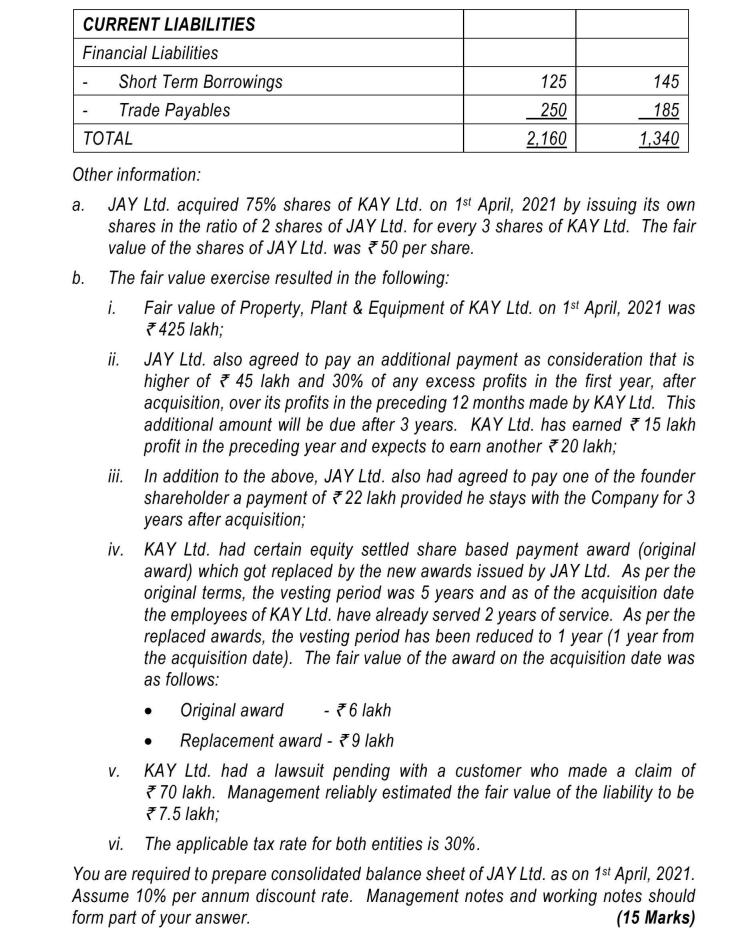

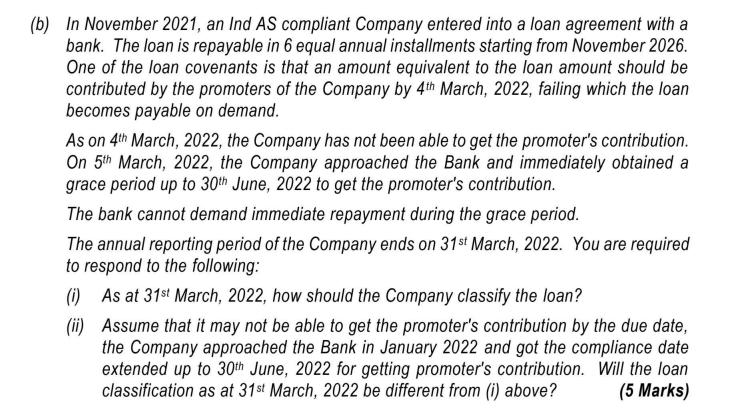

(a) The draft Balance Sheet of JAY Ltd. and KAY Ltd. as at 31st March 2021...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

(a) The draft Balance Sheet of JAY Ltd. and KAY Ltd. as at 31st March 2021 is given below: PARTICULARS JAY Limited KAY Limited (in lakh) (in lakh) ASSETS NON-CURRENT ASSETS Property, Plant & Equipment Investments CURRENT ASSETS Inventories Financial Assets - Trade Receivables Cash & Cash Equivalents Others TOTAL EQUITY AND LIABILITIES EQUITY Share Capital JAY Limited: Equity Shares of 10 each KAY Limited: Equity Shares of 100 each OTHER EQUITY NON-CURRENT LIABILITIES Financial Liabilities - Long Term Borrowings Long Term Provisions Deferred Tax 400 450 180 520 260 350 2,160 600 725 350 70 40 500 120 130 270 145 175 1,340 450 210 250 80 20 CURRENT LIABILITIES Financial Liabilities a. Short Term Borrowings Trade Payables b. TOTAL Other information: JAY Ltd. acquired 75% shares of KAY Ltd. on 1st April, 2021 by issuing its own shares in the ratio of 2 shares of JAY Ltd. for every 3 shares of KAY Ltd. The fair value of the shares of JAY Ltd. was 50 per share. The fair value exercise resulted in the following: i. Fair value of Property, Plant & Equipment of KAY Ltd. on 1st April, 2021 was *425 lakh; ii. 125 250 2,160 145 185 1,340 V. JAY Ltd. also agreed to pay an additional payment as consideration that is higher of 45 lakh and 30% of any excess profits in the first year, after acquisition, over its profits in the preceding 12 months made by KAY Ltd. This additional amount will be due after 3 years. KAY Ltd. has earned 15 lakh profit in the preceding year and expects to earn another 20 lakh; iii. In addition to the above, JAY Ltd. also had agreed to pay one of the founder shareholder a payment of 22 lakh provided he stays with the Company for 3 years after acquisition; iv. KAY Ltd. had certain equity settled share based payment award (original award) which got replaced by the new awards issued by JAY Ltd. As per the original terms, the vesting period was 5 years and as of the acquisition date the employees of KAY Ltd. have already served 2 years of service. As per the replaced awards, the vesting period has been reduced to 1 year (1 year from the acquisition date). The fair value of the award on the acquisition date was as follows: Original award - 76 lakh Replacement award - 9 lakh KAY Ltd. had a lawsuit pending with a customer who made a claim of 70 lakh. Management reliably estimated the fair value of the liability to be *7.5 lakh; vi. The applicable tax rate for both entities is 30%. You are required to prepare consolidated balance sheet of JAY Ltd. as on 1st April, 2021. Assume 10% per annum discount rate. Management notes and working notes should form part of your answer. (15 Marks) (b) In November 2021, an Ind AS compliant Company entered into a loan agreement with a bank. The loan is repayable in 6 equal annual installments starting from November 2026. One of the loan covenants is that an amount equivalent to the loan amount should be contributed by the promoters of the Company by 4th March, 2022, failing which the loan becomes payable on demand. As on 4th March, 2022, the Company has not been able to get the promoter's contribution. On 5th March, 2022, the Company approached the Bank and immediately obtained a grace period up to 30th June, 2022 to get the promoter's contribution. The bank cannot demand immediate repayment during the grace period. The annual reporting period of the Company ends on 31st March, 2022. You are required to respond to the following: (i) As at 31st March, 2022, how should the Company classify the loan? (ii) Assume that it may not be able to get the promoter's contribution by the due date, the Company approached the Bank in January 2022 and got the compliance date extended up to 30th June, 2022 for getting promoter's contribution. Will the loan classification as at 31st March, 2022 be different from (i) above? (5 Marks) (a) The draft Balance Sheet of JAY Ltd. and KAY Ltd. as at 31st March 2021 is given below: PARTICULARS JAY Limited KAY Limited (in lakh) (in lakh) ASSETS NON-CURRENT ASSETS Property, Plant & Equipment Investments CURRENT ASSETS Inventories Financial Assets - Trade Receivables Cash & Cash Equivalents Others TOTAL EQUITY AND LIABILITIES EQUITY Share Capital JAY Limited: Equity Shares of 10 each KAY Limited: Equity Shares of 100 each OTHER EQUITY NON-CURRENT LIABILITIES Financial Liabilities - Long Term Borrowings Long Term Provisions Deferred Tax 400 450 180 520 260 350 2,160 600 725 350 70 40 500 120 130 270 145 175 1,340 450 210 250 80 20 CURRENT LIABILITIES Financial Liabilities a. Short Term Borrowings Trade Payables b. TOTAL Other information: JAY Ltd. acquired 75% shares of KAY Ltd. on 1st April, 2021 by issuing its own shares in the ratio of 2 shares of JAY Ltd. for every 3 shares of KAY Ltd. The fair value of the shares of JAY Ltd. was 50 per share. The fair value exercise resulted in the following: i. Fair value of Property, Plant & Equipment of KAY Ltd. on 1st April, 2021 was *425 lakh; ii. 125 250 2,160 145 185 1,340 V. JAY Ltd. also agreed to pay an additional payment as consideration that is higher of 45 lakh and 30% of any excess profits in the first year, after acquisition, over its profits in the preceding 12 months made by KAY Ltd. This additional amount will be due after 3 years. KAY Ltd. has earned 15 lakh profit in the preceding year and expects to earn another 20 lakh; iii. In addition to the above, JAY Ltd. also had agreed to pay one of the founder shareholder a payment of 22 lakh provided he stays with the Company for 3 years after acquisition; iv. KAY Ltd. had certain equity settled share based payment award (original award) which got replaced by the new awards issued by JAY Ltd. As per the original terms, the vesting period was 5 years and as of the acquisition date the employees of KAY Ltd. have already served 2 years of service. As per the replaced awards, the vesting period has been reduced to 1 year (1 year from the acquisition date). The fair value of the award on the acquisition date was as follows: Original award - 76 lakh Replacement award - 9 lakh KAY Ltd. had a lawsuit pending with a customer who made a claim of 70 lakh. Management reliably estimated the fair value of the liability to be *7.5 lakh; vi. The applicable tax rate for both entities is 30%. You are required to prepare consolidated balance sheet of JAY Ltd. as on 1st April, 2021. Assume 10% per annum discount rate. Management notes and working notes should form part of your answer. (15 Marks) (b) In November 2021, an Ind AS compliant Company entered into a loan agreement with a bank. The loan is repayable in 6 equal annual installments starting from November 2026. One of the loan covenants is that an amount equivalent to the loan amount should be contributed by the promoters of the Company by 4th March, 2022, failing which the loan becomes payable on demand. As on 4th March, 2022, the Company has not been able to get the promoter's contribution. On 5th March, 2022, the Company approached the Bank and immediately obtained a grace period up to 30th June, 2022 to get the promoter's contribution. The bank cannot demand immediate repayment during the grace period. The annual reporting period of the Company ends on 31st March, 2022. You are required to respond to the following: (i) As at 31st March, 2022, how should the Company classify the loan? (ii) Assume that it may not be able to get the promoter's contribution by the due date, the Company approached the Bank in January 2022 and got the compliance date extended up to 30th June, 2022 for getting promoter's contribution. Will the loan classification as at 31st March, 2022 be different from (i) above? (5 Marks)

Expert Answer:

Related Book For

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these accounting questions

-

Bell Corporation purchases land by issuing its own common stock. How do we report this transaction, if at all?

-

The summarized balance sheet of Jay Ltd as on 31.12.06 and 31.12.2007 are as follows: Liabilities 2006 2007 Assets 2006 Share capital General Reserve Creditors Tax provision Prov. for doubtful debt...

-

Non Current Assets Property Plant & Machinery Investment in Kettle Current Assets Inventory Trade Receivables Current Account - Kettle Bank TOTAL ASSETS Equity & Liabilities Ordinary Share Capital 1...

-

Payroll Assignment - (50 Marks) The following employees are working in the ABC Clinic, they are paid biweekly. Calculate the gross income, net income, and the total remittance that ABC is to report...

-

Again consider the entity-relationship diagram shown in Figure. Add the following to the diagram and list any assumptions you had to make. A faculty member usually teaches many course sections, but...

-

Choose the best answer. 1. Colleges and universities look to which standard-setting body for GAAP? a. The GASB. b. The FASB. c. The NACUBO. d. It depends on whether the entity is public, private, or...

-

Prove that the order of convergence of the Crank-Nicolson finite difference method is \[O\left(\Delta x^{2}+\left(\frac{\Delta t}{2} ight)^{2} ight)\]

-

Gentle Bens Bar and Restaurant uses 5,000 quart bottles of an imported wine each year. The effervescent wine costs $ 3 per bottle and is served only in whole bottles because it loses its bubbles...

-

For your conclusion, describe how the concepts of diaspora and accretion change the way local communities are defined by global historical event?

-

3 Consider the following possible alternatives to the vector norms we encountered in the notes. For each, state whether the proposed definition satisfies the conditions of a norm or not. If it does,...

-

On March 1 , a concert promoter sells a summer season concert ticket for $ 1 , 0 0 0 . The season starts on May 1 and runs through September 3 0 . What accounts would be in the adjusting entry for...

-

SolarFlex produces the Flex 1 0 0 0 solar panel at a small factory located in the outskirts of Lake Country. The factory has equipment and machinery; some of which was purchased from a leading...

-

Crane Ltd. purchased a new machine on April 4, 2020, at a cost of $172,000. The company estimated that the machine would have a residual value of $14,000. The machine is expected to be used for...

-

July 12 Sold merchandise to Wally Butler, who paid the $1,060 purchase with cash. The goods cost Evergreen Company $630. July 15 Sold merchandise to Claudio's Chair Company at a selling price of...

-

Randall Company manufactures products to customer specifications. A job costing system is used to accumulate production costs. Factory overhead cost was applied at 125% of direct labor cost. Selected...

-

Consider a 9-month forward contract on 100 shares of stock when the stock price is $100. We assume that the risk-free interest rate continuously compounded is 10% per annum for all maturities. We...

-

Anne is employed by Bradley Contracting Company. Bradley has a $1.3 million contract to build a small group of outbuildings in a national park. Anne alleges that Bradley Contracting has discriminated...

-

The following are criticisms made of the IASB's 2015 exposure draft proposing updates to its Conceptual Framework. 1. The framework does not consider the meaning of the term 'true and fair view'...

-

Arnold plc and Bunny plc agreed to establish a Joint Operation, Carlton, which started trading on 1 January 20X1. Carlton is an unincorporated business, which is financed and managed by Arnold and...

-

The following are the summarized financial statements of two companies, Peel and Caval, for the financial year ended 31 October 2011. Income Statements for the year ended 31 October 2011 Statements...

-

Obtain the time variation of the lift and propulsive force coefficients and their plots for the airfoil given by Example 8.5. Assume that the profile pitches about quarter chord point. Example 8.5...

-

Write down a numerical solution algorithm for the LU decomposition solution of the pseudo penta diagonal matrix equation given by (A11.4). A11.4 || B C 2 A2 B2 C2 922 An-1 Bn-1 Cn-1 -1 An Bn R R Rn-1...

-

Obtain Eq. 8.66 as a relation between the wake vorticity and the reduced circulation. Eq. 8.66 w(x) = k(Q; cosx-22, sin x) cos ks +k(Q; sin x+Q, cos x) sinks, Q = Q, +Q;i

Study smarter with the SolutionInn App