Question: (a). The expectations theory provides a foundation for our understanding of interest rate determination. Outline the expectations theory approach to the determination of interest rates.

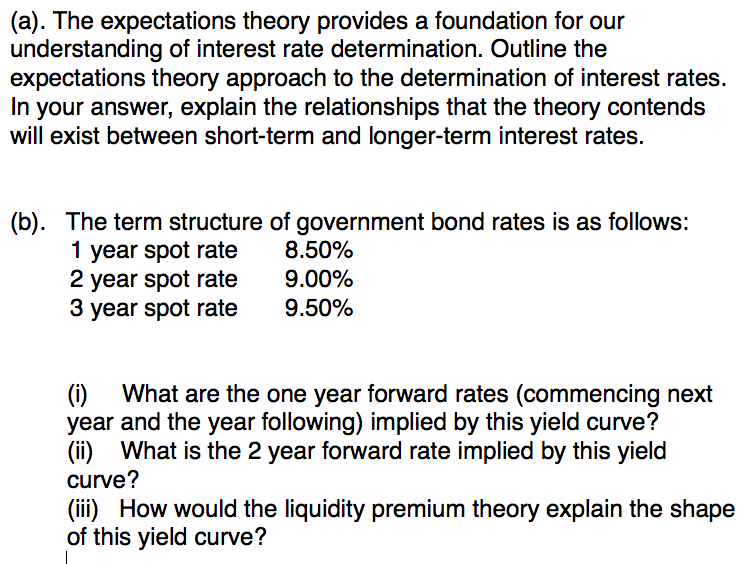

(a). The expectations theory provides a foundation for our understanding of interest rate determination. Outline the expectations theory approach to the determination of interest rates. In your answer, explain the relationships that the theory contends will exist between short-term and longer-term interest rates. (b). The term structure of government bond rates is as follows: 1 year spot rate 2 year spot rate 3 year spot rate 8.50% 9.00% 9.50% (i) What are the one year forward rates (commencing next year and the year following) implied by this yield curve? (ii) What is the 2 year forward rate implied by this yield curve? (ii) How would the liquidity premium theory explain the shape of this yield curve? (a). The expectations theory provides a foundation for our understanding of interest rate determination. Outline the expectations theory approach to the determination of interest rates. In your answer, explain the relationships that the theory contends will exist between short-term and longer-term interest rates. (b). The term structure of government bond rates is as follows: 1 year spot rate 2 year spot rate 3 year spot rate 8.50% 9.00% 9.50% (i) What are the one year forward rates (commencing next year and the year following) implied by this yield curve? (ii) What is the 2 year forward rate implied by this yield curve? (ii) How would the liquidity premium theory explain the shape of this yield curve

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts