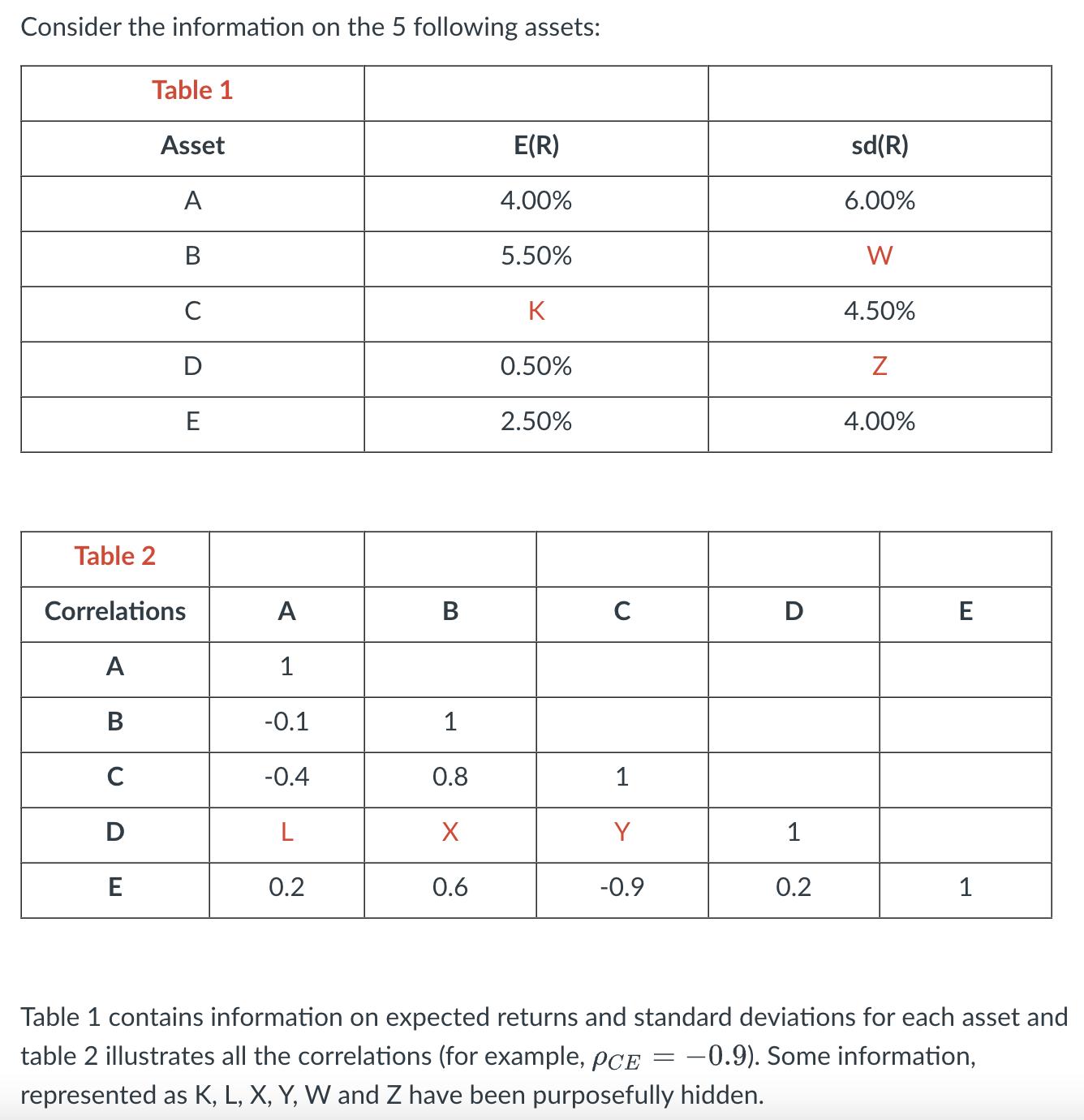

a) What values would Z and L assume if asset D is the risk-free asset. b) Calculate

Fantastic news! We've Found the answer you've been seeking!

Question:

a) What values would Z and L assume if asset D is the risk-free asset.

b) Calculate W given that it has the same Sharpe ratio as asset A.

c) Calculate the weights of the global minimum-variance portfolio formed by assets A and E only. Show the formula you used and the working out.

d) Indicate the approximate weights of the market portfolio involving assets A and E only. You don’t need to calculate them (or show any formulas), just providing the approximate values is sufficient, but explain how you obtained it.

Expert Answer:

Related Book For

Corporate Finance

ISBN: 978-0077861759

10th edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

Posted Date: