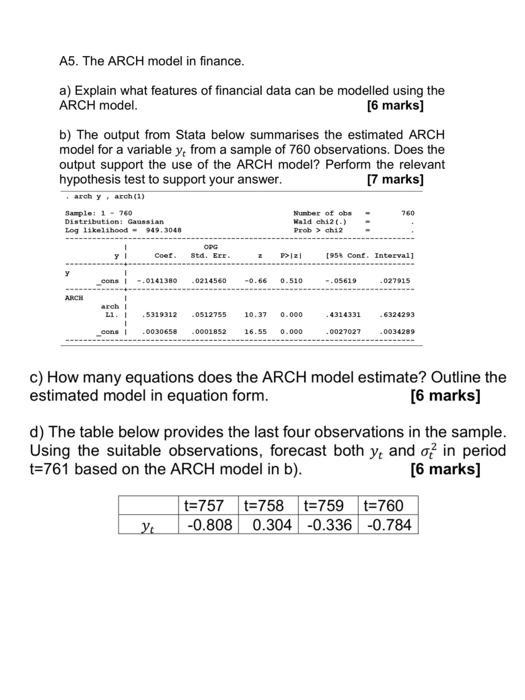

Question: A5. The ARCH model in finance. a) Explain what features of financial data can be modelled using the ARCH model. [6 marks] b) The

A5. The ARCH model in finance. a) Explain what features of financial data can be modelled using the ARCH model. [6 marks] b) The output from Stata below summarises the estimated ARCH model for a variable y, from a sample of 760 observations. Does the output support the use of the ARCH model? Perform the relevant hypothesis test to support your answer. [7 marks] archy, arch (1) Sample: 1 760 Distribution: Gaussian Log likelihood - 949.3048 y ARCH cons Coef. --0141380 OPG Std. Err. 0214560 arch I L1. I 5319312 cons I .0030658 0001852 Yt 2 -0.66 Number of obs Wald chi2 (-) Prob > ch12 P>|z| 0.510 0512755 10.37 0.000 16.55 0.000 1958 Conf. Interval] -.05619 4314331 760 -0027027 027915 .6324293 0034289 c) How many equations does the ARCH model estimate? Outline the estimated model in equation form. [6 marks] d) The table below provides the last four observations in the sample. Using the suitable observations, forecast both y, and of in period t=761 based on the ARCH model in b). [6 marks] t=757 t=758 t=759 t=760 -0.808 0.304 -0.336 -0.784

Step by Step Solution

3.38 Rating (167 Votes )

There are 3 Steps involved in it

STEP ... View full answer

Get step-by-step solutions from verified subject matter experts