Question: ACC 3113 Au ' 'ng case Analysis - Case report CASE STUDY - TEST 3 - Individual General description The Sportage Clothing Company has been

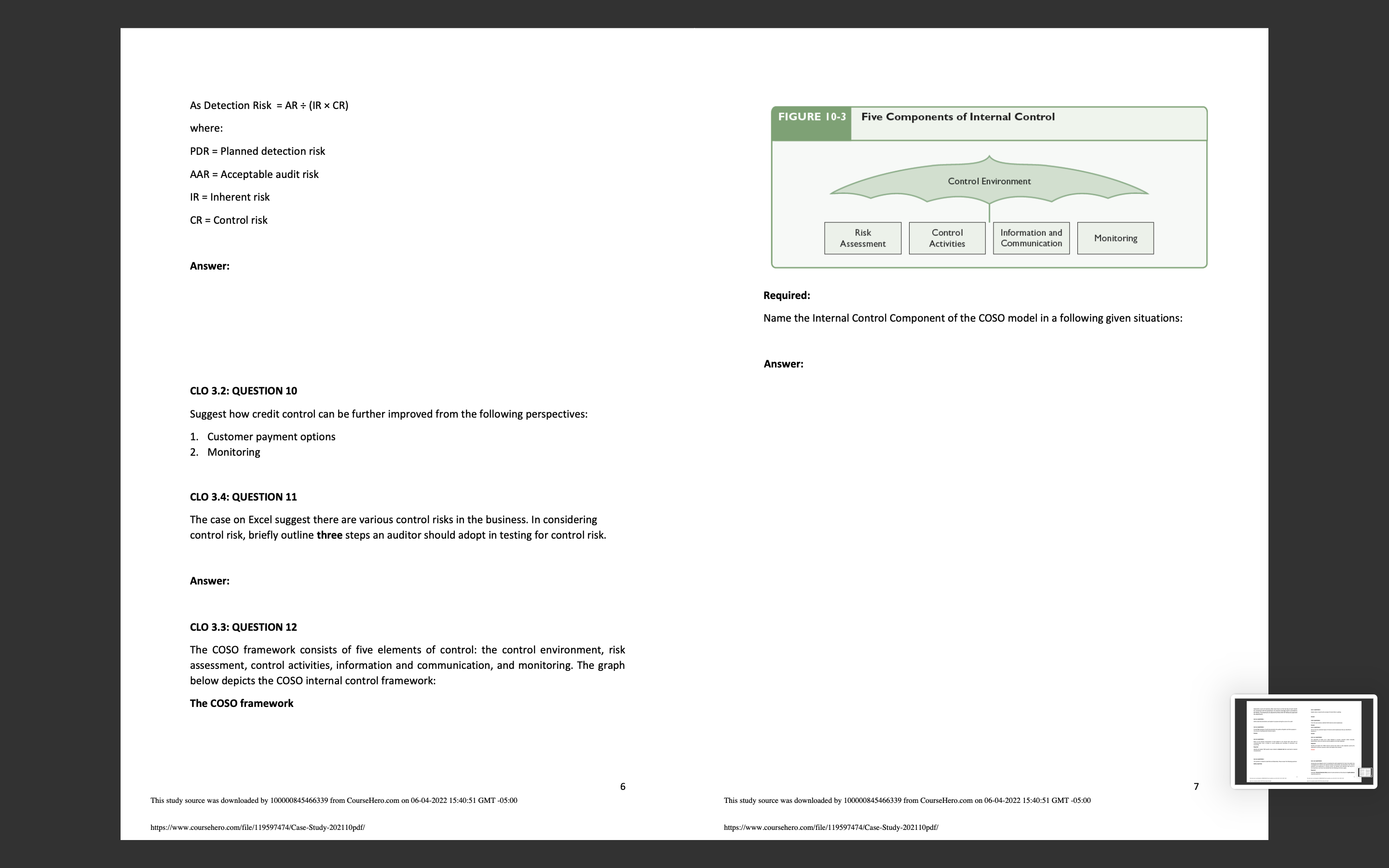

ACC 3113 Au ' 'ng case Analysis - Case report CASE STUDY - TEST 3 - Individual General description The Sportage Clothing Company has been trading for 18 years from its very large and only outlet in Abu Dhabi. The business is a retail store dealing in expensive open cloth and finished sports clothing. It has a staff of approximately 22 salesclerks and other 10 other admin staff. Sales transaction are completed on either cash or credit, using the store's own invoicing system rather than credit cards. Most of the larger sales are on credit. Only one central cash register is used, controlled by the store supervisor, Mr Saeed. The cash register is physically positioned to monitor the entire store and the front door. Mr Saeed has been working for Mr Rafeeq, the store owner, for over 16 years and is well aware of almost every aspect of the business, including finance and logistics. Customer Ordering Process Each salesclerk has his/her own manual sales book with pre-numbered, three- copy, multi-colored sales slips attached that are perforated. All transactions are recorded in the salesclerks' sales books. When the sale is for cash, the customer pays the salesclerks, who marks all three copies 'paid' and takes the money to the supervisor to process and complete the sales transaction. All transactions incur standard rate VAT. Errors in the Ordering Process The supervisor compares the clothing to the description on the invoice and the price on the sales tag. He also rechecks the clerk's calculations. Should there be any errors, then the corrections are approved by the salesclerk. The salesclerk 1m study mm wu mama by inmommzsu rm CourseHmAmn ml com-m2 mom GMT 4153 hltps'llwww mmmnmm l95974'mCmSludy-101l ledll amends his sales book at that time in front of the supervisor, and the items are packaged and given to the customer. Credit sales A credit sale must be approved by the supervisor from a list of approved credit customers after the salesclerk prepares the three-part invoice. Next, the supervisor enters the sale in his cash register as a credit (otherwise a cash sale is entered if credit facility is not granted to the customer). The second copy of the invoice, which has been validated by the cash register, is given to the customer. Mr Rafeeq must approve ALL credit sales that exceed US$1,200. Business bunklng procedure The cash is deposited in the bank the next morning by Mr Rafeeq, And he receives a deposit slip, which he gives to the accounts receivable clerk. If Mr Rafeeq is unable to deposit the money, the supervisor goes to the bank instead. Book-keeglng The salesclerks give their books to the supervisor at the end of each day, Mr Saeed, who compares the totals to the cash register tape and will then create a summary of the day's transactions. The cashier's copies of the invoices are also given to the accounts receivables clerk along with a summary of the day's receipts. Adnan, the accounts receivable clerk, reviews the sales books and the register tape. He inputs all the sales invoice information into the company/s computer, which provides a complete printout of all input and summaries. The accounting summary includes sales by the salesclerks, cash sales, credit sales and total sales. Adnan compares this output with the summary and reconciles all differences. The computer updates account receivable, inventory, and general ledger master les. After the update procedure has been run on the computer, Adnan's assistant les all sales included in the printout, Adnan uses these les to create transaction statements that are mailed to the customers. General Admin duties Mr Rafeeq's secretary opens the company mail each morning. She gives all correspondence to Mr Rafeeq and all payments to the supervisor. The supervisor totals the amounts and adds this cash to the register for later deposit. He gives the total to Adnan to update customer accounts on the computer. Adnan uses this list and all the remittances to record cash receipts and update accounts receivable, again by computer. He reconciles the total receipts on the pre-list to the deposit slip and to his printout. At the same time, Adnan compares the deposit slip received from the bank for cash sales to the cash receipts journal. He has online access to the store's bank account, which he accesses monthly to pay the store's bills online. The computer generates a weekly aged trial balance of the accounts receivable. A separate listing of all unpaid bills is also automatically prepared, and both are given to Mr Rafeeq. He approves all write-offs of uncollectible items and forwards the list to Adnan, who writes them off. Involclng Each month Adnan mails computer-generated statements to customers. Any customer complaints and disagreements are resolved by Mr Rafeeq, who then informs Adnan, in writing, of any write-downs or misstatements that require correction. The computer system also automatically totals the journals and posts the totals to the general ledger. A general ledger trial balance is printed out, from which Adnan prepares financial statements. Reconciliations and other duties Adnan also prepares monthly bank reconciliations and reconciles the general ledger to the aged accounts receivables trial balance. Because the importance of inventry control, Adnan prints out the inventory perpetual totals monthly, on the last day of each moth. This study mm m downloaded by immisszsu from motel-(memo on 06414-2022 15:40:\" GMT .053 1a.; may mum w downloaded by immuwmzsa from Coumlhocom on 06-04-2012 15:40:\" GMT om) hltps'llwww mammal/malll959'747'lCmSludy-11llopdl/ bltps'Nwww ammonia/ler! |95Wl1ucne~5|udy~1l11l lopdll Salesclerks count all inventory after store hours on the last day of each month CLO 2: QUESTION 5 for comparison with the perpetuals. An inventory shortage report is provided to Mr Rafeeq. The perpetuals are adjusted by Adnan after Mr Rafeeq has approved Explain what is meant by the concept of Control Risk in auditing the adjustments. Answer CLO 2.6: QUESTION 1 CLO2: QUESTION 6 Define Audit documentations and explain its purpose during the course of an audit From the case scenario, identify FOUR internal control weaknesses Answer CLO 2.6: QUESTION 2 CLO 2: QUESTION 7 Provide four examples of audit documentation the auditor will gather and their purpose in Discuss the four potential impact of internal control weaknesses that you identified in the process of auditing Excels financial reports Question 6 Answer: Answer CLO 2.12: QUESTION 8 CLO 2.8: QUESTION 3 The salesclerks at Excels use a Sales Daybook to process customer orders manually. Much of the business environment of Excel appears to be manual with some level of Nevertheless, there are internal controls applied to the Sales Daybooks. computerization that is limited to record keeping and recording of transaction and Required: accounting Identify and explain the THREE internal controls that relate to sales daybooks used by the Required: salesclerks to process customer orders and explain their purpose Identify and explain TWO specific issues related to inherent risk that could lead to material Answer: misstatements CLO 2.8: QUESTION 4 This question is related to Audit Risk and Materiality. Please answer the following questions: CLO 2.10: QUESTION 9 Define Audit Risk Having done due diligence prior to accepting the audit assignment for Excel, the auditor has investigated the internal and external business environment and factored-in the inherent weakness and weaknesses in internal control. He believes that Detection Risk may be a worrying factor and hence has decided that the following risk factors apply: Required: Calculate: Planned Detection Risk (column 5) and comment on the amount of audit evidence required (column 6) This study source was downloaded by 100000845466339 from CourseHero.com on 06-04-2022 15:40:51 GMT -05:00 This study source was downloaded by 100000845466339 from CourseHero.com on 06-04-2022 15:40:51 GMT -05:00 https://www.coursehero.com/file/1 19597474/Case-Study-2021 10pdf/ https://www.coursehero.com/file/1 19597474/Case-Study-2021 10pdf/As Detection Risk = AR : (IR x CR) FIGURE 10-3 Five Components of Internal Control where: PDR = Planned detection risk AAR = Acceptable audit risk Control Environment IR = Inherent risk CR = Control risk Risk Control Information and Assessment Activities Communication Monitoring Answer: Required: Name the Internal Control Component of the COSO model in a following given situations: Answer: CLO 3.2: QUESTION 10 Suggest how credit control can be further improved from the following perspectives: 1. Customer payment options 2. Monitoring CLO 3.4: QUESTION 11 The case on Excel suggest there are various control risks in the business. In considering control risk, briefly outline three steps an auditor should adopt in testing for control risk. Answer: CLO 3.3: QUESTION 12 The COSO framework consists of five elements of control: the control environment, risk assessment, control activities, information and communication, and monitoring. The graph below depicts the COSO internal control framework The COSO framework This study source was downloaded by 100000845466339 from CourseHero.com on 06-04-2022 15:40:51 GMT -05:00 This study source was downloaded by 100000845466339 from CourseHero.com on 06-04-2022 15:40:51 GMT -05:00 https://www.coursehero.com/file/1 19597474/Case-Study-2021 10pdf/ https:/www.coursehero.com/file/1 19597474/Case-Study-2021 10pdf/

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!