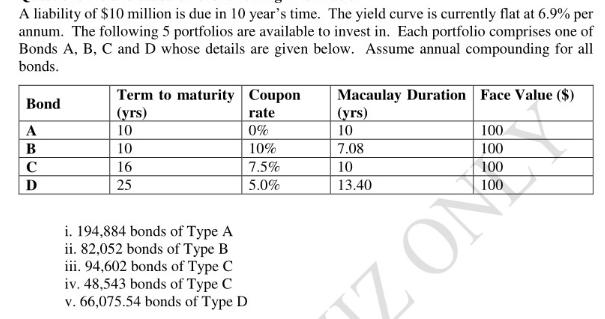

1). Which of the following portfolios is suitable for immunizing this liability against a shift in interest...

Fantastic news! We've Found the answer you've been seeking!

Question:

1). Which of the following portfolios is suitable for immunizing this liability against a shift in interest rates today:

A). Portfolio (i)

B). Portfolio (ii)

C). Portfolio (iii)

D). Portfolio (iv)

E). Portfolio (v)

2). You consider immunizing against the liability by investing in 66,075.54 bonds of Type D. This portfolio has a present value, today, equal to the present value of the liability. If the yield curve increases to 7.9%, what is the new present value of this immunizing portfolio?

A). 4,813,754.96

B). 4,806,248.87

C). 4,544,469.09

D). 4,531,608.71

E). None of the above

Expert Answer:

Related Book For

Posted Date: