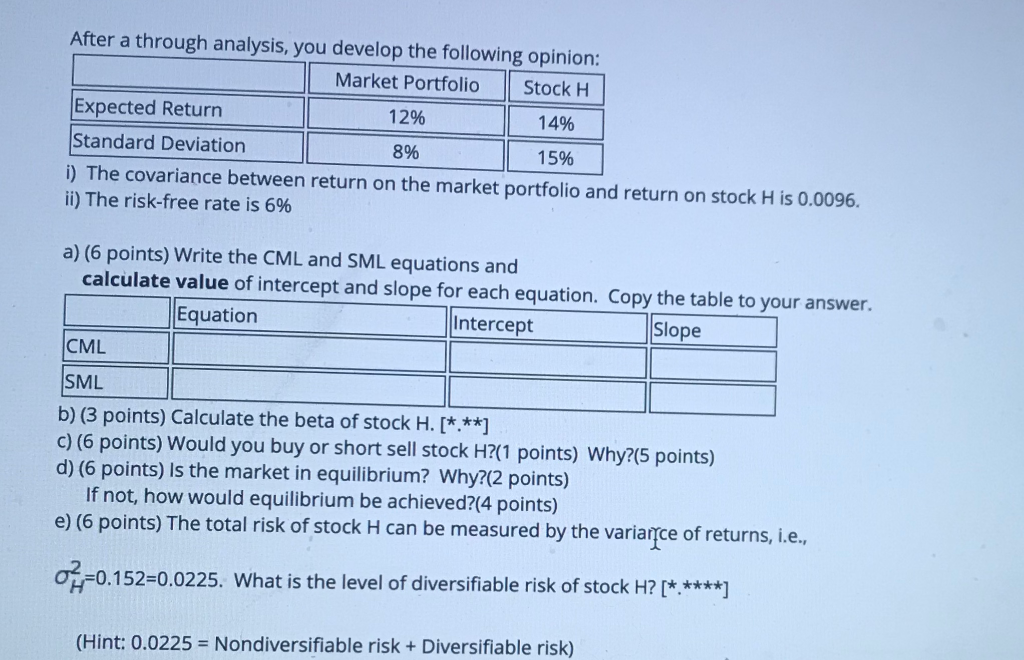

Question: After a through analysis, you develop the following opinion: Market Portfolio Stock H Expected Return 12% 14% Standard Deviation 8% 15% i) The covariance between

After a through analysis, you develop the following opinion: Market Portfolio Stock H Expected Return 12% 14% Standard Deviation 8% 15% i) The covariance between return on the market portfolio and return on stock H is 0.0096. ii) The risk-free rate is 6% a) (6 points) Write the CML and SML equations and calculate value of intercept and slope for each equation. Copy the table to your answer. Equation Intercept Slope CML SML b) (3 points) Calculate the beta of stock H. [***] c) (6 points) Would you buy or short sell stock H?(1 points) Why?(5 points) d) (6 points) Is the market in equilibrium? Why?(2 points) If not, how would equilibrium be achieved?(4 points) e) (6 points) The total risk of stock H can be measured by the variarce of returns, i.e., ox=0.152=0.0225. What is the level of diversifiable risk of stock H? [*****] (Hint: 0.0225 = Nondiversifiable risk + Diversifiable risk) After a through analysis, you develop the following opinion: Market Portfolio Stock H Expected Return 12% 14% Standard Deviation 8% 15% i) The covariance between return on the market portfolio and return on stock H is 0.0096. ii) The risk-free rate is 6% a) (6 points) Write the CML and SML equations and calculate value of intercept and slope for each equation. Copy the table to your answer. Equation Intercept Slope CML SML b) (3 points) Calculate the beta of stock H. [***] c) (6 points) Would you buy or short sell stock H?(1 points) Why?(5 points) d) (6 points) Is the market in equilibrium? Why?(2 points) If not, how would equilibrium be achieved?(4 points) e) (6 points) The total risk of stock H can be measured by the variarce of returns, i.e., ox=0.152=0.0225. What is the level of diversifiable risk of stock H? [*****] (Hint: 0.0225 = Nondiversifiable risk + Diversifiable risk)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts