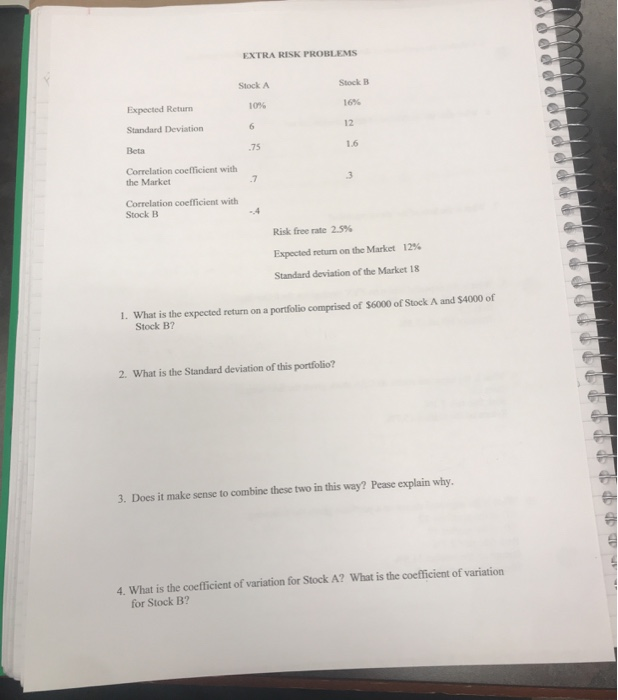

Question: EXTRA RISK PROBLEMS Stock A Stock B Expected Return 10% 16% Standard Deviation Correlation coefficient with the Market Correlation coefficient with Stock B Risk free

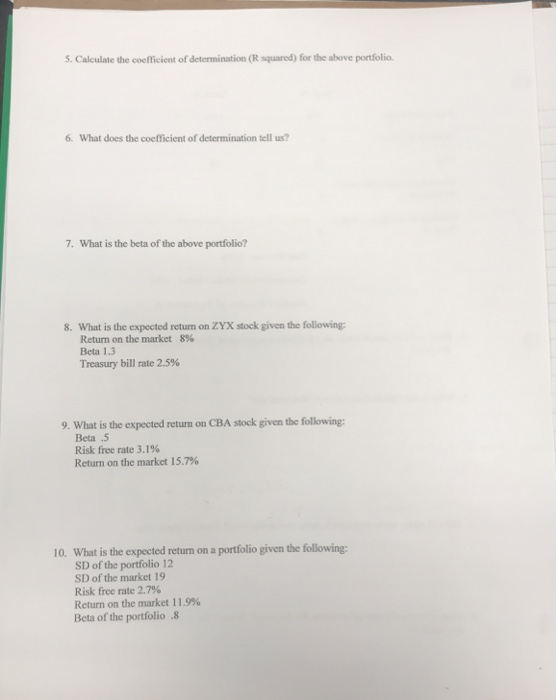

EXTRA RISK PROBLEMS Stock A Stock B Expected Return 10% 16% Standard Deviation Correlation coefficient with the Market Correlation coefficient with Stock B Risk free rate 25% Expected return on the Market 12% Standard deviation of the Market 18 1. What is the expected return on a portfolio comprised of $6000 of Stock A and $4000 of Stock B? 2. What is the Standard deviation of this portfolio? 3. Does it make sense to combine these two in this way? Pease explain why. 4. What is the coefficient of variation for Stock A? What is the coefficient of variation for Stock B? 5. Calculate the coefficient of determination (R squared) for the above portfolio 6. What does the coefficient of determination tell us? 7. What is the beta of the above portfolio? 8. What is the expected return on ZYX stock given the following: Return on the market 8% Beta 1.3 Treasury bill rate 2.5% 9. What is the expected return on CBA stock given the following: Beta .5 Risk free rate 3.1% Return on the market 15.7% 10. What is the expected return on a portfolio given the following: SD of the portfolio 12 SD of the market 19 Risk free rate 2.7% Return on the market 11.9% Beta of the portfolio .8

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts