Question: also prepare all consolidated entries needed to prepare a full set of consolidated financial statements at December 31, 20X5 for putt and slice b. Prepare

also prepare all consolidated entries needed to prepare a full set of consolidated financial statements at December 31, 20X5 for putt and slice

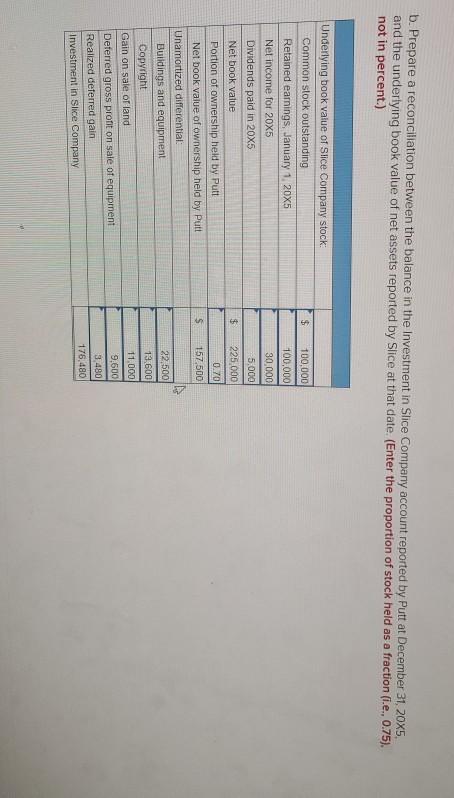

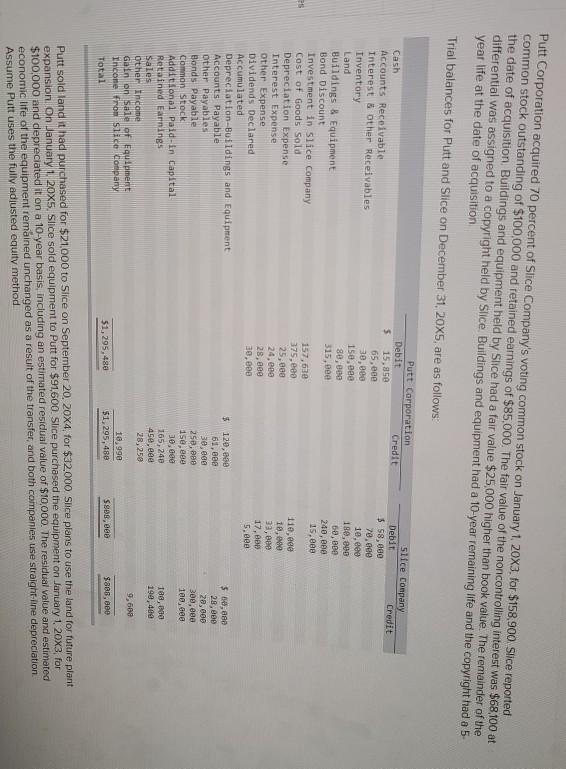

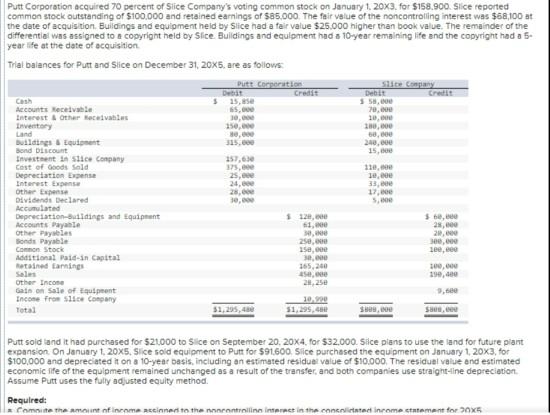

b. Prepare a reconciliation between the balance in the Investment in Slice Company account reported by Putt at December 31, 20X5 and the underlying book value of net assets reported by Slice at that date. (Enter the proportion of stock held as a fraction (i.e., 0.75). not in percent.) $ Underlying book value of Slice Company stock Common stock outstanding Retained earnings, January 1 20X5 Nel income for 20X5 Dividends paid in 20X5 Net book value Portion of ownership held by Putt Net book value of ownership held by Putt Unamortized differential: Buildings and equipment Copyright Gain on sale or land Deferred gross profit on sale of equipment Realized deferred gain Investment in Slice Company 100,000 100,000 30.000 5,000 225.000 0.70 157,500 $ S 22,500 13.600 11.000 9,600 3.480 176,480 Putt Corporation acquired 70 percent of Slice Company's voting common stock on January 1 20x3 for $158,900 Slice reported common stock outstanding of $100,000 and retained earnings of $85,000. The fair value of the noncontrolling interest was $68,100 at the date of acquisition Buildings and equipment held by Slice had a fair value $25,000 higher than book value. The remainder of the differential was assigned to a copyright held by Slice Buildings and equipment had a 10-year remaining life and the copyright had a 5 year life at the date of acquisition Trial balances for Putt and Slice on December 31, 20X5, are as follows: 5 Putt Corporation Debit Credit 15,850 65,000 30,000 158, eee se, es 315, cea Slice Company Debit Credit $ 58,800 70.ee 10, een 180,000 68,000 240,00 15.ee 25 Cash Accounts Receivable Interest & Other Receivables Inventory Land Buildings & Equipment Bond Discount Investment in Slice Company Cost of Goods Sold Depreciation Expense Interest Expense Other Expense Dividends Declared Accumulated Depreciation-Buildings and Equipment Accounts Payable other payables Bonds Payable Common Stock Additional Paid in Capital Retained Earnings Sales Other Income Gain on sale of Equipment Incone from Slice Company Total 157,630 375,00 25,000 24.ee 28,00 3e, 11e, eee 18, 33, Bee 17.00 5.000 $ 120,00 61,00 3e, esa 250,00 150,00 30,000 165, 240 45e,eee 28,250 $ 60,000 28,888 20,000 300,eee 100, see Tag, a 190, 400 9,600 16,990 $1,295,488 51,295,488 $908,888 $888, Bee Putt sold land it had purchased for $21,000 to Slice on September 20, 20X4, for $32,000. Slice plans to use the land for future plant expansion On January 1, 20X5. Slice sold equipment to Putt for $91,600. Slice purchased the equipment on January 1 20x3 for $100,000 and depreciated it on a 10-year basis, including an estimated residual value of $10,000. The residual value and estimated economic life of the equipment remained unchanged as a result of the transfer, and both companies use straight-line depreciation. Assume Putt uses the fully adjusted equity method an Putt Corporation acquired 70 percent of Slice Company's voting common stock on January 1, 20X3. for $158.900. Slice reported common stock outstanding of $100.000 and retained earnings of $85.000 The fair value of the noncontrolling interest was $68,100 at the date of acquisition Buildings and equipment held by Slice had a fair value $25.000 higher than book value. The remainder of the differential was assigned to copyright held by Slice Buildings and equipment had a 10-year remaining life and the copyright had a 5. year life at the date of acquisition Trial balances for Putt and slice on December 31, 20X5. are as follows: Dutt sports Site Company Credit Credit Cash 5 15,se $ 58,00 Accounts receive 65.000 70.00 Interest other receivables 10, 10, 20,00 58,00 Buildings at 240,000 Bond Discount 15. Investment in slice Company 157,63 Cost of Goods Sold 37, 120.000 Depreciation Expanse 10, Interest Expense 24.00 33, Other Expense 17,00 Dividends Declared 30,00 Accumulated Depreciation tidings and Equipment Accounts Payante $1,000 28,000 Other Payables 20,000 Bonds Payable 250,000 300.000 Additional Paidan Capital 25e,ce 200,00 30,000 atained taming 165,240 Sales 100,000 45,000 Other Income 199,00 Gain on sale of equipment Income from Slice Company 10.000 Total 51,295, Su,200 Saeco Putt sold and it had purchased for 521000 to Sice on September 20, 20X4. for $32,000. Sice plans to use the land for future plant expansion On January 1, 20X5. Slice sold equipment to Putt for $91.600 Silice purchased the equipment on January 1, 20X3, for $100,000 and deprecated it on a 10-year basis, including an estimated residus value of $10.000 The residual value and estimated economic life of the equipment remained unchanged as a result of the transfer and both companies use straight-line depreciation Assume Putt uses the fully adjusted equity method Required: Camote the amount of income actinners to the controllin interest in the contented income statement for 10X5 b. Prepare a reconciliation between the balance in the Investment in Slice Company account reported by Putt at December 31, 20X5 and the underlying book value of net assets reported by Slice at that date. (Enter the proportion of stock held as a fraction (i.e., 0.75). not in percent.) $ Underlying book value of Slice Company stock Common stock outstanding Retained earnings, January 1 20X5 Nel income for 20X5 Dividends paid in 20X5 Net book value Portion of ownership held by Putt Net book value of ownership held by Putt Unamortized differential: Buildings and equipment Copyright Gain on sale or land Deferred gross profit on sale of equipment Realized deferred gain Investment in Slice Company 100,000 100,000 30.000 5,000 225.000 0.70 157,500 $ S 22,500 13.600 11.000 9,600 3.480 176,480 Putt Corporation acquired 70 percent of Slice Company's voting common stock on January 1 20x3 for $158,900 Slice reported common stock outstanding of $100,000 and retained earnings of $85,000. The fair value of the noncontrolling interest was $68,100 at the date of acquisition Buildings and equipment held by Slice had a fair value $25,000 higher than book value. The remainder of the differential was assigned to a copyright held by Slice Buildings and equipment had a 10-year remaining life and the copyright had a 5 year life at the date of acquisition Trial balances for Putt and Slice on December 31, 20X5, are as follows: 5 Putt Corporation Debit Credit 15,850 65,000 30,000 158, eee se, es 315, cea Slice Company Debit Credit $ 58,800 70.ee 10, een 180,000 68,000 240,00 15.ee 25 Cash Accounts Receivable Interest & Other Receivables Inventory Land Buildings & Equipment Bond Discount Investment in Slice Company Cost of Goods Sold Depreciation Expense Interest Expense Other Expense Dividends Declared Accumulated Depreciation-Buildings and Equipment Accounts Payable other payables Bonds Payable Common Stock Additional Paid in Capital Retained Earnings Sales Other Income Gain on sale of Equipment Incone from Slice Company Total 157,630 375,00 25,000 24.ee 28,00 3e, 11e, eee 18, 33, Bee 17.00 5.000 $ 120,00 61,00 3e, esa 250,00 150,00 30,000 165, 240 45e,eee 28,250 $ 60,000 28,888 20,000 300,eee 100, see Tag, a 190, 400 9,600 16,990 $1,295,488 51,295,488 $908,888 $888, Bee Putt sold land it had purchased for $21,000 to Slice on September 20, 20X4, for $32,000. Slice plans to use the land for future plant expansion On January 1, 20X5. Slice sold equipment to Putt for $91,600. Slice purchased the equipment on January 1 20x3 for $100,000 and depreciated it on a 10-year basis, including an estimated residual value of $10,000. The residual value and estimated economic life of the equipment remained unchanged as a result of the transfer, and both companies use straight-line depreciation. Assume Putt uses the fully adjusted equity method an Putt Corporation acquired 70 percent of Slice Company's voting common stock on January 1, 20X3. for $158.900. Slice reported common stock outstanding of $100.000 and retained earnings of $85.000 The fair value of the noncontrolling interest was $68,100 at the date of acquisition Buildings and equipment held by Slice had a fair value $25.000 higher than book value. The remainder of the differential was assigned to copyright held by Slice Buildings and equipment had a 10-year remaining life and the copyright had a 5. year life at the date of acquisition Trial balances for Putt and slice on December 31, 20X5. are as follows: Dutt sports Site Company Credit Credit Cash 5 15,se $ 58,00 Accounts receive 65.000 70.00 Interest other receivables 10, 10, 20,00 58,00 Buildings at 240,000 Bond Discount 15. Investment in slice Company 157,63 Cost of Goods Sold 37, 120.000 Depreciation Expanse 10, Interest Expense 24.00 33, Other Expense 17,00 Dividends Declared 30,00 Accumulated Depreciation tidings and Equipment Accounts Payante $1,000 28,000 Other Payables 20,000 Bonds Payable 250,000 300.000 Additional Paidan Capital 25e,ce 200,00 30,000 atained taming 165,240 Sales 100,000 45,000 Other Income 199,00 Gain on sale of equipment Income from Slice Company 10.000 Total 51,295, Su,200 Saeco Putt sold and it had purchased for 521000 to Sice on September 20, 20X4. for $32,000. Sice plans to use the land for future plant expansion On January 1, 20X5. Slice sold equipment to Putt for $91.600 Silice purchased the equipment on January 1, 20X3, for $100,000 and deprecated it on a 10-year basis, including an estimated residus value of $10.000 The residual value and estimated economic life of the equipment remained unchanged as a result of the transfer and both companies use straight-line depreciation Assume Putt uses the fully adjusted equity method Required: Camote the amount of income actinners to the controllin interest in the contented income statement for 10X5

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts