a. An investor buys a 4.4% annual coupon payment bond with six years to maturity. The bond

Fantastic news! We've Found the answer you've been seeking!

Question:

a. An investor buys a 4.4% annual coupon payment bond with six years to maturity. The bond has a yield-to-maturity of 6%. The par value is $1000.

i. Determine the market price of the bond.

ii. Calculate the bond’s duration and modified duration.

iii. If the YTM decreases to 5.5%, what is the predicted dollar change in price using the duration concept?

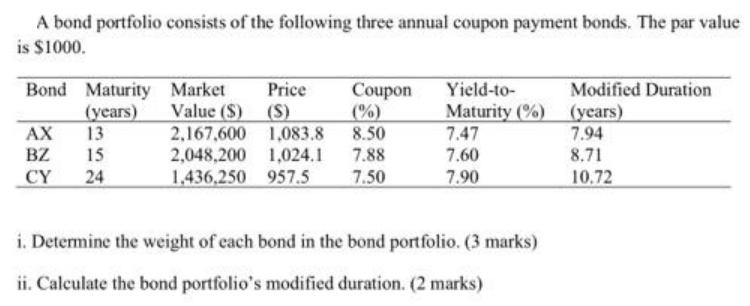

b

Expert Answer:

Related Book For

Posted Date: