Question: ANSWER ALL THE QUESTIONS IN BOTH SECTION A & SECTION B. SECTION A (50 Marks) QUESTION ONE (25 Marks) Imagine you have E100 000 to

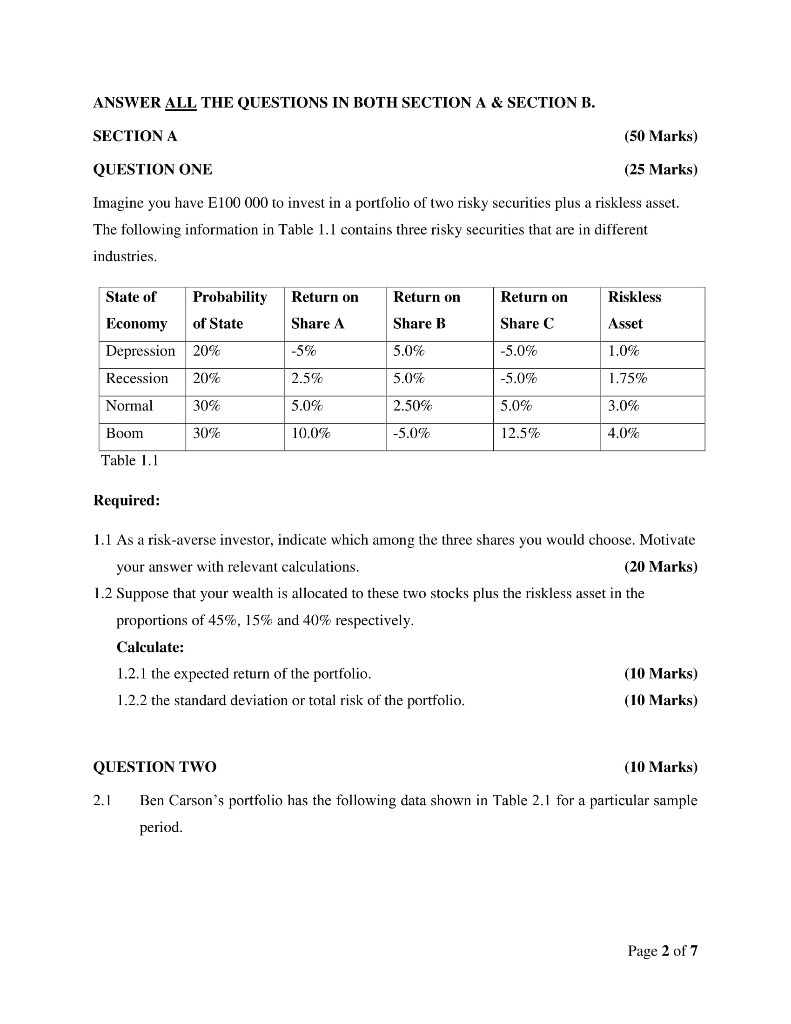

ANSWER ALL THE QUESTIONS IN BOTH SECTION A & SECTION B. SECTION A (50 Marks) QUESTION ONE (25 Marks) Imagine you have E100 000 to invest in a portfolio of two risky securities plus a riskless asset. The following information in Table 1.1 contains three risky securities that are in different industries. Return on Riskless State of Economy Depression Recession Normal Asset Probability of State 20% 20% 30% Return on Share A -5% 2.5% 5.0% Return on Share B 5.0% Share C -5.0% -5.0% 5.0% 12.5% 1.0% 1.75% 5.0% 2.50% 3.0% Boom 30% 10.0% -5.0% 4.0% Table 1.1 Required: 1.1 As a risk-averse investor, indicate which among the three shares you would choose. Motivate your answer with relevant calculations. (20 Marks) 1.2 Suppose that your wealth is allocated to these two stocks plus the riskless asset in the proportions of 45%, 15% and 40% respectively. Calculate: 1.2.1 the expected return of the portfolio. (10 Marks) 1.2.2 the standard deviation or total risk of the portfolio. (10 Marks) QUESTION TWO (10 Marks) 2.1 Ben Carson's portfolio has the following data shown in Table 2.1 for a particular sample period. Page 2 of 7

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts