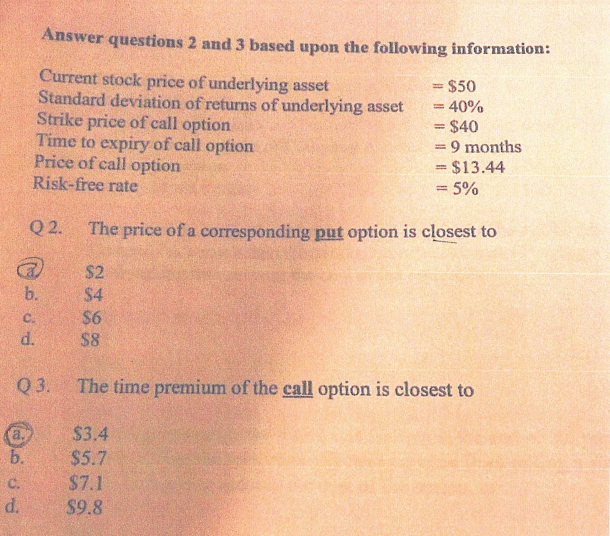

Question: Answer questions 2 and 3 based upon the following information: Current stock price of underlying asset Standard deviation of returns of underlying asset Strike price

Answer questions 2 and 3 based upon the following information: Current stock price of underlying asset Standard deviation of returns of underlying asset Strike price of call option Time to expiry of call option Price of call option Risk-free rate $50 4 $40 - 9 months $13.44 02. The price of a corresponding put option is closest to b. $4 c $6 d. S8 The time premium of the call option is closest to Q3. S3.4 b. $5.7 $7.1 d. S9.8

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock