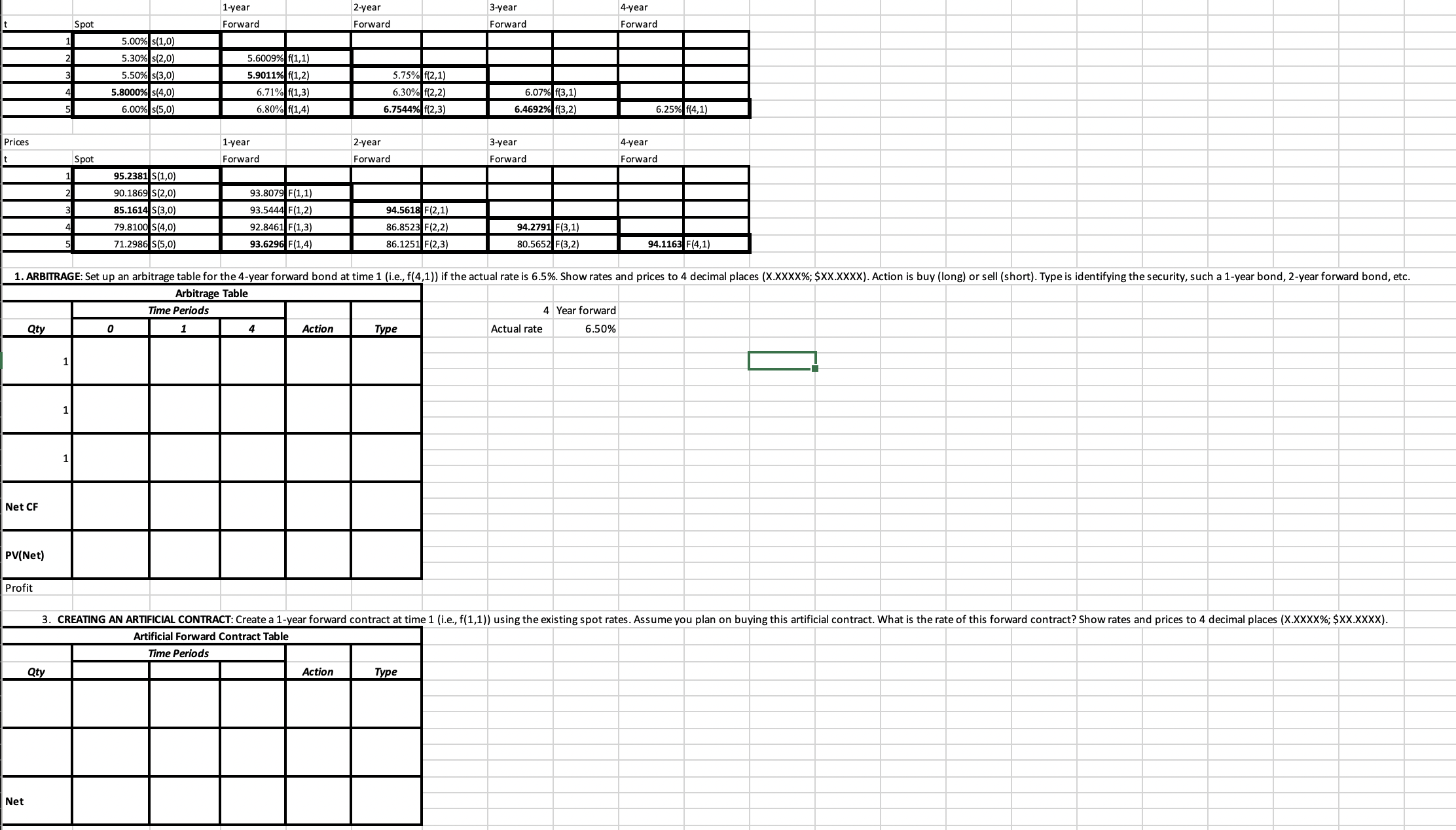

Question: ARBITRAGE: Set up an arbitrage table for the 4 - year forward bond at time 1 ( i . e . , f ( 4

ARBITRAGE: Set up an arbitrage table for the year forward bond at time ie f if the actual rate is Show rates and prices to decimal places XXXXX; $XXXXXX Action is buy long or sell short Type is identifying the security, such a year bond, year forward bond, etc.

CREATING AN ARTIFICIAL CONTRACT: Create a year forward contract at time ie f using the existing spot rates. Assume you plan on buying this artificial contract. What is the rate of this forward contract? Show rates and prices to decimal places XXXXX; $XXXXXX

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock