Question: As discussed in Section 8.3, the Markowitz model uses the variance of the portfolio as the measure of risk. However, variance includes deviations both below

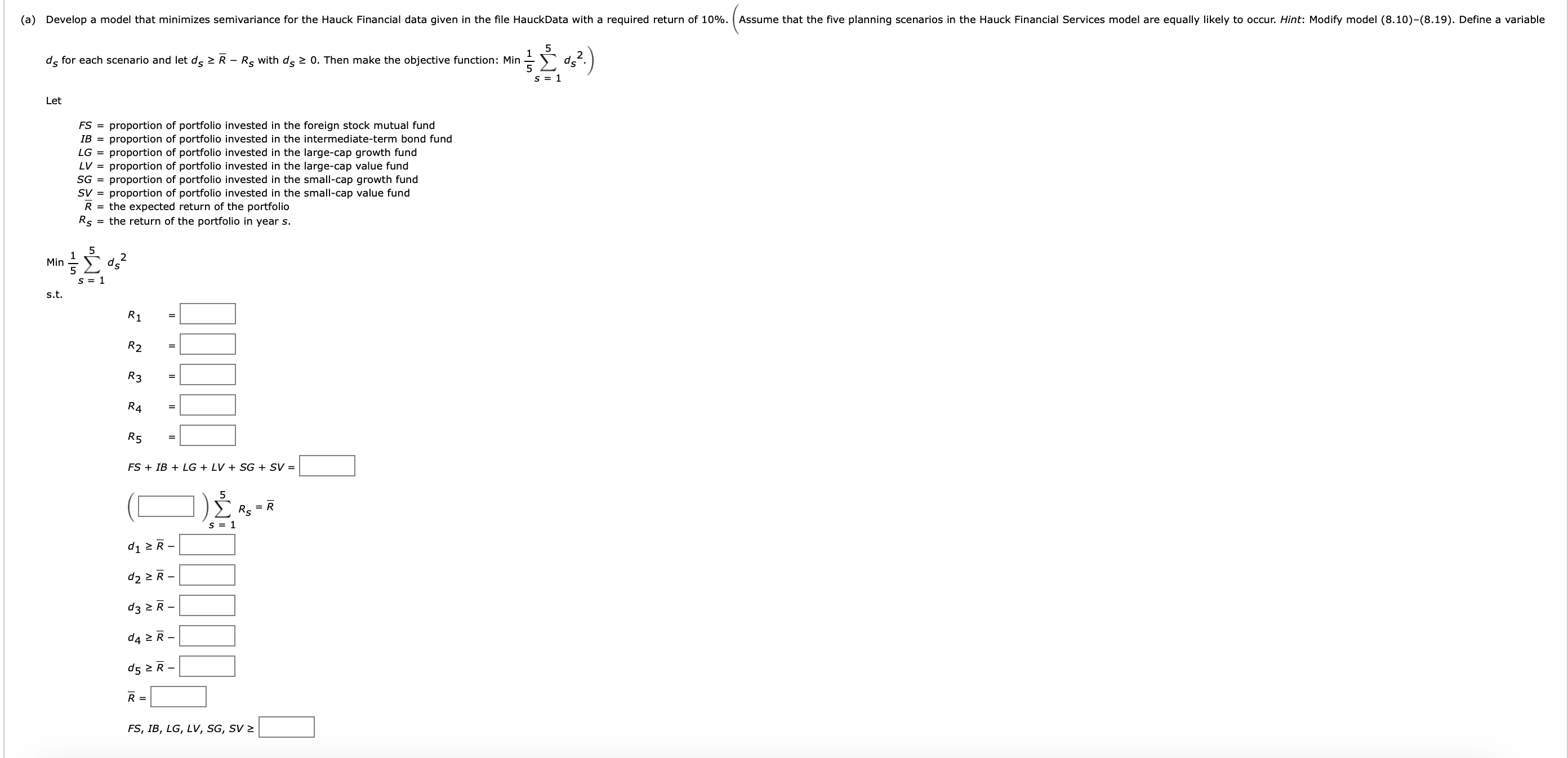

As discussed in Section 8.3, the Markowitz model uses the variance of the portfolio as the measure of risk. However, variance includes deviations both below and above the mean return. Semivariance includes only deviations below the mean and is considered by many to be a better measure of risk.

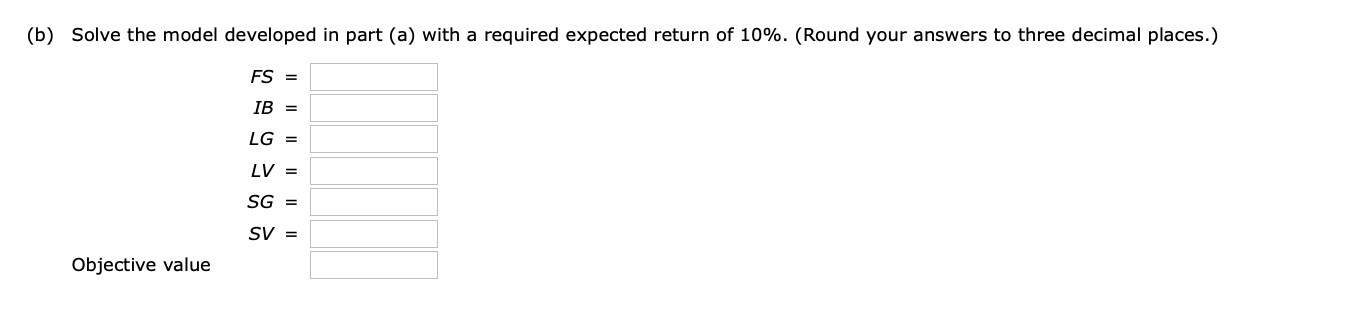

ds for each scenario and let dsRRs with ds0. Then make the objective function: Min 51s=15ds2.) Let FSIB=proportionofportfolioinvestedintheforeignstockmutualfund=proportionofportfolioinvestedintheintermediate-termbondfund IBLG=proportionofportfolioinvestedintheintermediate-termbond=proportionofportfolioinvestedinthelarge-capgrowthfund LG= proportion of portfolio invested in the large-cap growth fund LV= proportion of portfolio invested in the large-cap value fund SG= proportion of portfolio invested in the small-cap growth fund SV= proportion of portfolio invested in the small-cap value fund RRS=theexpectedreturnoftheportfolio=thereturnoftheportfolioinyears. Min51s=15ds2 s.t. R1=R2= R3=R4=R5=FS+IB+LG+V+SG+SV=()s=15Rs=Rd1Rd2Rd3Rd4Rd5RR= FS,IB,LG,LV,SG,SV (b) Solve the model developed in part (a) with a required expected return of 10%. (Round your answers to three decimal places.) FS=IB=LG=LV=SG=SV= Objective value ds for each scenario and let dsRRs with ds0. Then make the objective function: Min 51s=15ds2.) Let FSIB=proportionofportfolioinvestedintheforeignstockmutualfund=proportionofportfolioinvestedintheintermediate-termbondfund IBLG=proportionofportfolioinvestedintheintermediate-termbond=proportionofportfolioinvestedinthelarge-capgrowthfund LG= proportion of portfolio invested in the large-cap growth fund LV= proportion of portfolio invested in the large-cap value fund SG= proportion of portfolio invested in the small-cap growth fund SV= proportion of portfolio invested in the small-cap value fund RRS=theexpectedreturnoftheportfolio=thereturnoftheportfolioinyears. Min51s=15ds2 s.t. R1=R2= R3=R4=R5=FS+IB+LG+V+SG+SV=()s=15Rs=Rd1Rd2Rd3Rd4Rd5RR= FS,IB,LG,LV,SG,SV (b) Solve the model developed in part (a) with a required expected return of 10%. (Round your answers to three decimal places.) FS=IB=LG=LV=SG=SV= Objective value

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts