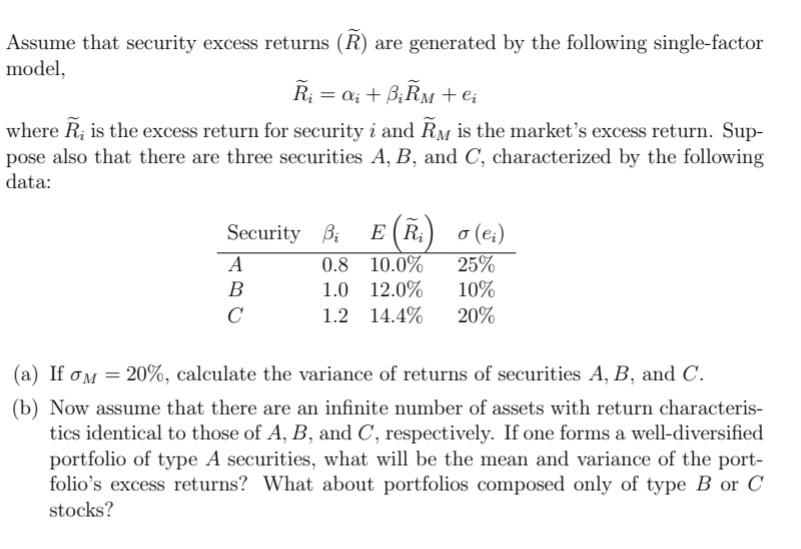

Question: Assume that security excess returns (R) are generated by the following single-factor model, ; = 0; + B;M + tei where ; is the excess

Assume that security excess returns (R) are generated by the following single-factor model, ; = 0; + B;M + tei where ; is the excess return for security i and n is the market's excess return. Sup- pose also that there are three securities A, B, and C, characterized by the following data: Security Bi E (R) A 0.8 10.0% B 1.0 12.0% 1.2 14.4% o(ei) 25% 10% 20% (a) If om = 20%, calculate the variance of returns of securities A, B, and C. (b) Now assume that there are an infinite number of assets with return characteris- tics identical to those of A, B, and C, respectively. If one forms a well-diversified portfolio of type A securities, what will be the mean and variance of the port- folio's excess returns? What about portfolios composed only of type B or C stocks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts