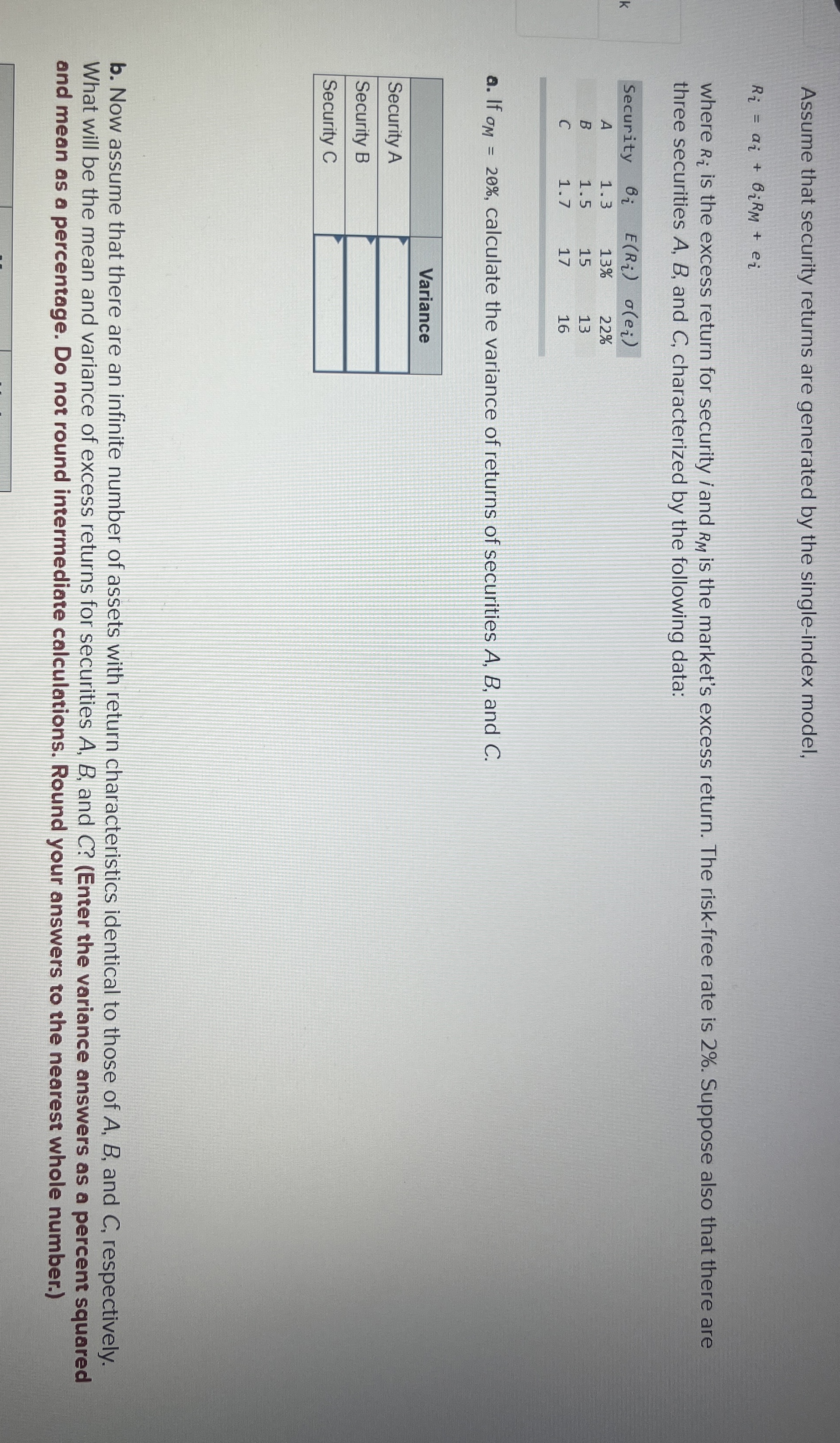

Question: Assume that security returns are generated by the single - index model, R i = a i + i R M + e i where

Assume that security returns are generated by the singleindex model,

where is the excess return for security i and is the market's excess return. The riskfree rate is Suppose also that there are three securities and characterized by the following data:

tableSecurity

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock