Assume you work for a consultancy firm specialized in the provision of management accounting related services. You

Question:

Assume you work for a consultancy firm specialized in the provision of management accounting related services. You have been appointed to work on a new project that involves recommending pricing strategies for Nature Candle'ssenior management team.

Around 750 words are required.

It should be designed to recommend pricing strategies for Nature Candle's products, in consideration of its market position and external environment.

The following text is part of the case study thst is the relevant to the question.

After this, some work has been down in the previous project assignment is listed, which might be helpful to the new project.

The Case of Nature Candle Limited

Nature Candle Limited is a medium-sized Australian- owned manufacturer of candles based in Richmond, Victoria. It specialises in the production of quality candles for the wholesale and retail markets. Following the "eco-friendly" value, Nature Candle Limited only produces candles made of natural ingredients, such as

soy wax and beeswax, with cotton or linen wicks. Their customers range from household candle lovers to a broad range of corporate and boutique companies that are proud to put their labels on the customised candles.

The market of candles is traditionally dominated by paraffin candles made of paraffin wax - a petroleum by-product refined from crude oil that is also commonly used in beauty products. However, increasing research in recent years show that paraffin candles, particularly those with artificial scents and dyes, are potentially hazardous to users, causing damage to the brain, lung and central nerve system. Hence, more and more candle manufacturers turn their eyes to the eco-friendly candle segment. With its long-standing expertise in the design and production of high-quality soy wax and beeswax candles, unique ability to meet customer's individual needs and flexibility with specific requirements of different demanding markets, Nature Candle is able to compete with larger local manufacturers in the segment.

James Bright, a Monash commerce graduate who has recently been employed by Nature Candle Limited, was asked by the CEO of Nature Candle to review the company's cost accounting procedures. In outlining this project to Bright, the CEO expressed three concerns about the present system:

1. Its adequacy for purposes of cost control

2. Its accuracy in arriving at the true cost of products

3. Its usefulness in providing data to judge employee and departmental performance

The CEO is keen to resolve these issues due to certain realities in Nature Candle's external environment. In addition to the increasing competition with larger Australian candle manufacturers, the signing of free trade agreements, such as Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), has also opened the gate for candles, lower in price, manufactured in South East Asia. While Nature Candle traditionally does not compete with other players on price, the pressure of lower-priced imports on the eco-friendly candle market is being felt by the company.

......

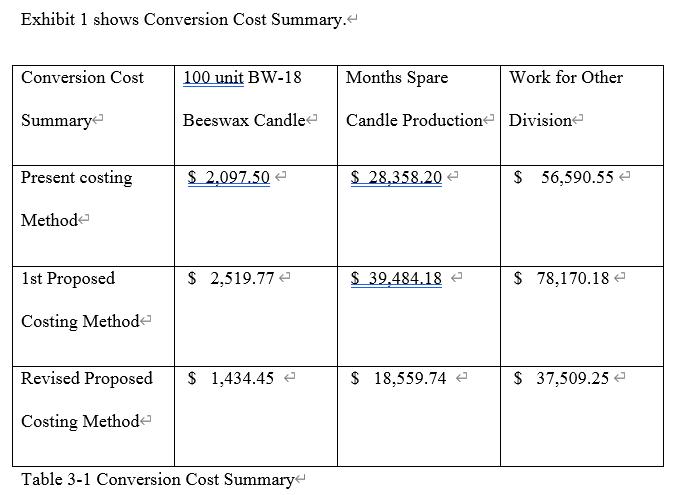

To obtain some concrete numbers to show the CEO, Bright decided to apply the proposed approach to three MCT activities: 1) the production of BW-18 beeswax candles (MCT's best- selling product); 2) production of spare candles for inventory, and 3) work done by MCT for other Nature Candle divisions. Exhibit 3 summarises the hourly requirements of these activities by department. Bright then costed these three activities using both the October plant-wide rate and the pro forma October departmental rates.

Upon seeing Bright's numbers, the CEO noted that there was large difference in the indicated cost of BW-18 beeswax candle as calculated under the present and proposed methods. The present method was, therefore, probably leading to incorrect inferences about the profitability of each product, the CEO surmised. The impact of the proposed method on spare candle inventory valuation was similarly noted. The CEO, therefore, leaned towards adopting the new method, but told Bright that the department managers should be consulted before any plans are made.

///////////////////////////////////////

Work has been down in previous assignment:

1.There is the conversion cost of a 100-unit batch of BW-18 beeswax candle, a month's production of spare candles for inventory, and a month's work done for other divisions under the present model, Bright's first proposal, and his revised proposal.

2.Assume that direct materials cost for a 100-unit batch of BW-18 beeswax candle is

$2,200 and that Nature Candle sells these candles at $46 each. Using both the present and first proposed costing methods, advise if the BW-18 price should be increased? Should it be dropped from the product line?

Answer:

3.1 Analysis on BW-18 price change and whether be dropped from the product line

3.2.1 1st Analysis

Based on the quantitative figures calculated if the present costing method is used there is no need to increase price since selling price is greater than the product cost or there is profit in every unit of BW-18.The higher the gross profit per unit the better for the firm since it will generate more possible income in every unit sold. But under the proposed costing method the price should be increase since the product cost is higher than the selling price. And if this costing method is used then the BW-18 will only incur loss if the price will not be increased.

3.2.2 2nd Analysis

Since there are two scenario's the decision will be different due to different product cost per unit under each costing method. Under present costing method BW-18 should not be dropped since it is profitable based on the difference of selling price and product cost per unit. Since there is positive difference in the present costing method product line should be continued since it will be profitable. Under the proposed costing method the product line selling price must increase in order to the product line to continue so that BW-18 will be profitable.

Expert Answer:

In the light of prevailing conditions in external environment of company the company should use competitive pricing strategy Competitive pricing is a strategy where company makes pricing decision base... View the full answer

Taxes and Business Strategy A Planning Approach

ISBN: 9780132752671

5th edition

Authors: Myron Scholes, Mark Wolfson, Merle Erickson, Michelle Hanlon