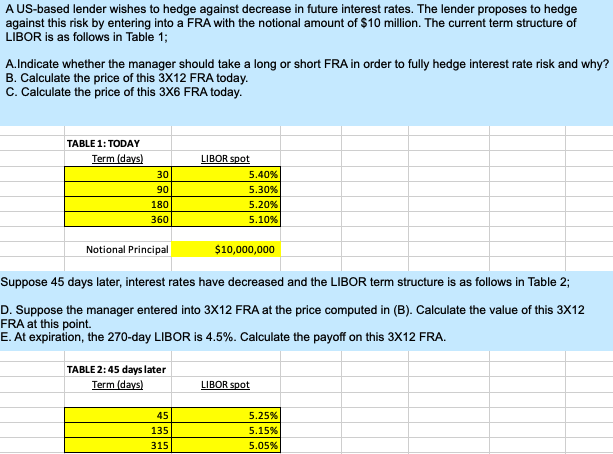

Question: AUS-based lender wishes to hedge against decrease in future interest rates. The lender proposes to hedge against this risk by entering into a FRA with

AUS-based lender wishes to hedge against decrease in future interest rates. The lender proposes to hedge against this risk by entering into a FRA with the notional amount of $10 million. The current term structure of LIBOR is as follows in Table 1; A.Indicate whether the manager should take a long or short FRA in order to fully hedge interest rate risk and why? B. Calculate the price of this 3X12 FRA today. C. Calculate the price of this 3X6 FRA today. TABLE 1: TODAY Term (days) 30 90 180 360 LIBOR spot 5.40% 5.30% 5.20% 5.10% Notional Principal $10,000,000 Suppose 45 days later, interest rates have decreased and the LIBOR term structure is as follows in Table 2; D. Suppose the manager entered into 3X12 FRA at the price computed in (B). Calculate the value of this 3X12 FRA at this point. E. At expiration, the 270-day LIBOR is 4.5%. Calculate the payoff on this 3X12 FRA. TABLE 2:45 days later Term (days) LIBOR spot 45 135 315 5.25% 5.15% 5.05%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts