Awethu (Pty) Ltd is a manufacturing company that has 31 December as its financial year-end. The...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

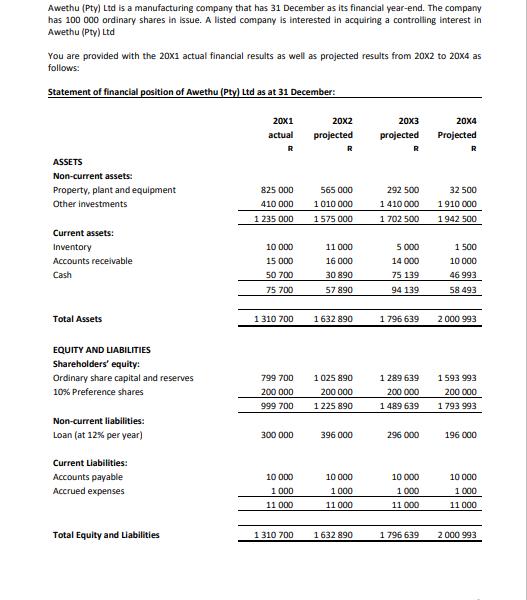

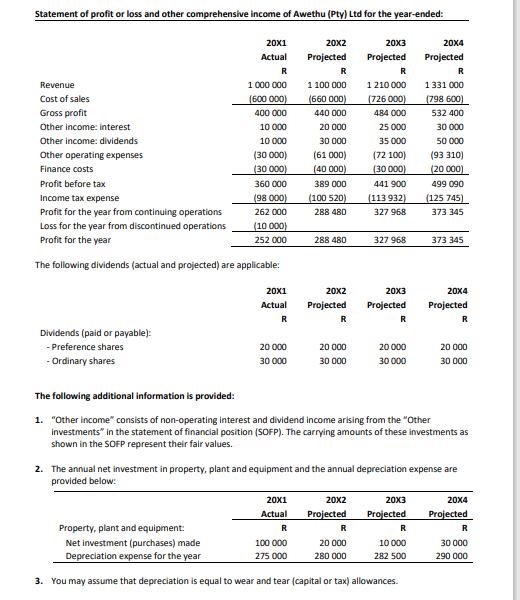

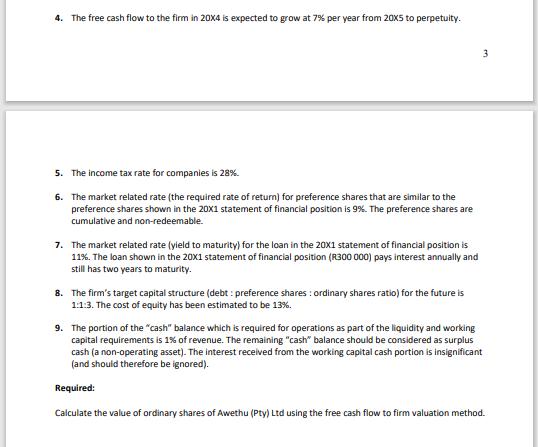

Awethu (Pty) Ltd is a manufacturing company that has 31 December as its financial year-end. The company has 100 000 ordinary shares in issue. A listed company is interested in acquiring a controlling interest in Awethu (Pty) Ltd You are provided with the 20X1 actual financial results as well as projected results from 20x2 to 20x4 as follows: Statement of financial position of Awethu (Pty) Ltd as at 31 December: ASSETS Non-current assets: Property, plant and equipment Other investments Current assets: Inventory Accounts receivable Cash Total Assets EQUITY AND LIABILITIES Shareholders' equity: Ordinary share capital and reserves 10% Preference shares Non-current liabilities: Loan (at 12% per year) Current Liabilities: Accounts payable Accrued expenses Total Equity and Liabilities 20x1 actual R 825 000 410 000 1 235 000 10 000 15 000 50 700 75 700 1 310 700 799 700 200 000 999 700 300 000 10 000 1000 11 000 1 310 700 20x2 projected R 565 000 1 010 000 1575 000 11 000 16 000 30 890 57 890 1632 890 1025 890 200 000 1225 890 396 000 10 000 1000 11 000 1632 890 20X3 projected R 292 500 1 410 000 1 702 500 5 000 14 000 75 139 94 139 1 796 639 1 289 639 200 000 1 489 639 296 000 10 000 1000 11 000 1 796 639 20X4 Projected R 32 500 1910 000 1942 500 1 500 10 000 46 993 58 493 2 000 993 1593 993 200 000 1 793 993 196 000 10 000 1.000 11 000 2 000 993 Statement of profit or loss and other comprehensive income of Awethu (Pty) Ltd for the year-ended: Revenue Cost of sales Gross profit Other income: interest Other income: dividends Other operating expenses Finance costs 20x1 Actual Dividends (paid or payable): - Preference shares - Ordinary shares R 1 000 000 (600 000) 400 000 10 000 10 000 000) (30 (30 000) Profit before tax Income tax expense Profit for the year from continuing operations Loss for the year from discontinued operations Profit for the year The following dividends (actual and projected) are applicable: 360 000 (98 000) 262 000 (10 000) 252 000 20X1 Actual R 20 000 30 000 20x2 Projected R 1 100 000 (660 000) 440 000 20 000 000 20x1 Actual R 100 000 275 000 30 (61 000) (40 000) 389 000 (100 520) 288 480 288 480 20x2 Projected R 20 000 30 000 20x2 Projected 20x3 Projected R 1 210 000 (726 000) 484 000 25 000 R 35 000 (72 100) (30 000) 441 900 (113 932) 327 968 20 000 280 000 327 968 20x3 Projected R 20 000 30 000 Property, plant and equipment: Net investment (purchases) made Depreciation expense for the year 3. You may assume that depreciation is equal to wear and tear (capital or tax) allowances. The following additional information is provided: 1. "Other income" consists of non-operating interest and dividend income arising from the "Other investments in the statement of financial position (SOFP). The carrying amounts of these investments as shown in the SOFP represent their fair values. 20x3 Projected 20X4 Projected 2. The annual net investment in property, plant and equipment and the annual depreciation expense are provided below: R 1331 000 (798 600) 532 400 30 000 R 10 000 282 500 50 000 (93 310) (20 000) 499 090 (125 745) 373 345 373 345 20X4 Projected R 20 000 30 000 20X4 Projected R 30 000 290 000 4. The free cash flow to the firm in 20X4 is expected to grow at 7% per year from 20x5 to perpetuity. 5. The income tax rate for companies is 28%. 6. The market related rate (the required rate of return) for preference shares that are similar to the preference shares shown in the 20X1 statement of financial position is 9%. The preference shares are cumulative and non-redeemable. 7. The market related rate (yield to maturity) for the loan in the 20X1 statement of financial position is 11%. The loan shown in the 20x1 statement of financial position (R300 000) pays interest annually and still has two years to maturity. 8. The firm's target capital structure (debt: preference shares ordinary shares ratio) for the future is 1:1:3. The cost of equity has been estimated to be 13%. 3 9. The portion of the "cash" balance which is required for operations as part of the liquidity and working capital requirements is 1% of revenue. The remaining "cash" balance should be considered as surplus cash (a non-operating asset). The interest received from the working capital cash portion is insignificant (and should therefore be ignored). Required: Calculate the value of ordinary shares of Awethu (Pty) Ltd using the free cash flow to firm valuation method. Awethu (Pty) Ltd is a manufacturing company that has 31 December as its financial year-end. The company has 100 000 ordinary shares in issue. A listed company is interested in acquiring a controlling interest in Awethu (Pty) Ltd You are provided with the 20X1 actual financial results as well as projected results from 20x2 to 20x4 as follows: Statement of financial position of Awethu (Pty) Ltd as at 31 December: ASSETS Non-current assets: Property, plant and equipment Other investments Current assets: Inventory Accounts receivable Cash Total Assets EQUITY AND LIABILITIES Shareholders' equity: Ordinary share capital and reserves 10% Preference shares Non-current liabilities: Loan (at 12% per year) Current Liabilities: Accounts payable Accrued expenses Total Equity and Liabilities 20x1 actual R 825 000 410 000 1 235 000 10 000 15 000 50 700 75 700 1 310 700 799 700 200 000 999 700 300 000 10 000 1000 11 000 1 310 700 20x2 projected R 565 000 1 010 000 1575 000 11 000 16 000 30 890 57 890 1632 890 1025 890 200 000 1225 890 396 000 10 000 1000 11 000 1632 890 20X3 projected R 292 500 1 410 000 1 702 500 5 000 14 000 75 139 94 139 1 796 639 1 289 639 200 000 1 489 639 296 000 10 000 1000 11 000 1 796 639 20X4 Projected R 32 500 1910 000 1942 500 1 500 10 000 46 993 58 493 2 000 993 1593 993 200 000 1 793 993 196 000 10 000 1.000 11 000 2 000 993 Statement of profit or loss and other comprehensive income of Awethu (Pty) Ltd for the year-ended: Revenue Cost of sales Gross profit Other income: interest Other income: dividends Other operating expenses Finance costs 20x1 Actual Dividends (paid or payable): - Preference shares - Ordinary shares R 1 000 000 (600 000) 400 000 10 000 10 000 000) (30 (30 000) Profit before tax Income tax expense Profit for the year from continuing operations Loss for the year from discontinued operations Profit for the year The following dividends (actual and projected) are applicable: 360 000 (98 000) 262 000 (10 000) 252 000 20X1 Actual R 20 000 30 000 20x2 Projected R 1 100 000 (660 000) 440 000 20 000 000 20x1 Actual R 100 000 275 000 30 (61 000) (40 000) 389 000 (100 520) 288 480 288 480 20x2 Projected R 20 000 30 000 20x2 Projected 20x3 Projected R 1 210 000 (726 000) 484 000 25 000 R 35 000 (72 100) (30 000) 441 900 (113 932) 327 968 20 000 280 000 327 968 20x3 Projected R 20 000 30 000 Property, plant and equipment: Net investment (purchases) made Depreciation expense for the year 3. You may assume that depreciation is equal to wear and tear (capital or tax) allowances. The following additional information is provided: 1. "Other income" consists of non-operating interest and dividend income arising from the "Other investments in the statement of financial position (SOFP). The carrying amounts of these investments as shown in the SOFP represent their fair values. 20x3 Projected 20X4 Projected 2. The annual net investment in property, plant and equipment and the annual depreciation expense are provided below: R 1331 000 (798 600) 532 400 30 000 R 10 000 282 500 50 000 (93 310) (20 000) 499 090 (125 745) 373 345 373 345 20X4 Projected R 20 000 30 000 20X4 Projected R 30 000 290 000 4. The free cash flow to the firm in 20X4 is expected to grow at 7% per year from 20x5 to perpetuity. 5. The income tax rate for companies is 28%. 6. The market related rate (the required rate of return) for preference shares that are similar to the preference shares shown in the 20X1 statement of financial position is 9%. The preference shares are cumulative and non-redeemable. 7. The market related rate (yield to maturity) for the loan in the 20X1 statement of financial position is 11%. The loan shown in the 20x1 statement of financial position (R300 000) pays interest annually and still has two years to maturity. 8. The firm's target capital structure (debt: preference shares ordinary shares ratio) for the future is 1:1:3. The cost of equity has been estimated to be 13%. 3 9. The portion of the "cash" balance which is required for operations as part of the liquidity and working capital requirements is 1% of revenue. The remaining "cash" balance should be considered as surplus cash (a non-operating asset). The interest received from the working capital cash portion is insignificant (and should therefore be ignored). Required: Calculate the value of ordinary shares of Awethu (Pty) Ltd using the free cash flow to firm valuation method.

Expert Answer:

Answer rating: 100% (QA)

WORKINGS WO Calculating WACC Debt Preference shares Ordinary shares WACC Corporate Financial Managem... View the full answer

Related Book For

Accounting

ISBN: 978-1118608227

9th edition

Authors: Lew Edwards, John Medlin, Keryn Chalmers, Andreas Hellmann, Claire Beattie, Jodie Maxfield, John Hoggett

Posted Date:

Students also viewed these general management questions

-

You are provided with the following information for Mondello Inc. Mondello Inc. uses the periodic method of accounting for its inventory transactions. March 1 Beginning inventory 2,000 liters at a...

-

You are provided with the following information for Merrell Enterprises, effective as of its April 30, 2012, year-end. Accounts payable ........... $ 834 Accounts receivable ........... 810...

-

You are provided with the following information for Rapp Corporation, effective as of its April 30, 2012, year-end. Accounts payable ........... $ 2,100 Accounts receivable ........... 9,150...

-

Sketch the six graphs of the x- and y-components of position, velocity, and acceleration versus time for projectile motion with x 0 = y 0 = 0 and 0 < 0 < 90.

-

Which measurements currently reported in balance sheets is not consistent with the physical capital maintenance concept? Give examples.

-

Sheet steel emerging from the hot roll section of a steel mill has a temperature of \(1000 \mathrm{~K}\), a thickness of \(\delta=2.5 \mathrm{~mm}\), and the following distribution for the spectral,...

-

In a review engagement, the independent accountant's procedures include: a. Examining bank reconciliations. b. Confirming accounts receivable with debtors. c. Reading the financial statements to...

-

Hicks Corporation seeks your assistance in developing cash and other budget information for August, September, and October. At July 30, the company had cash of $5,500, accounts receivable of...

-

In light of what you have learned about existing doctrine and the competing interests at stake, consider whether you are satisfied with the law's current approach, and, if not, try to identify...

-

1. Fill the missing values in the table and show the calculations. 2. Provide a detailed description of the Fresnel Zone and how it is affecting the condition of the link between the two sites. 3....

-

Short Essay Format: Please write several or more sentences in a paragraph for each question. Q1) Explain the term "modern machine". Q2) Explain the high-level meaning of input, Output, Processing,...

-

Please answer each given questions by number. Note : Please cite legal basis. 1. To celebrate his 15th birthday, actor Abe, who has made a fortune at a young age, wanted to buy Bob's vintage car. Bob...

-

A 5 3 2 nm pulse laser source produces a train of laser pulses with a 1 0 mJ energy at a 1 0 0 Hz repetition rate and a 1 0 nsec pulse width. How many photons are contained in each pulse? If the...

-

Morrow Corporation had only one job in process during May-Job X32Z-and had no finished goods inventory on May 1. Job X was started in April and finished during May, Data concerning that job appear...

-

First, take the Interpersonal Skills Self-Assessment found at the following weblink:Interpersonal Skills Self-Assessment Make a note of which of the four areas (listening skills, verbal...

-

2. Solve the following system of equations using Gauss elimination method. x+y+z = 9 2x+5y + 7z = 52 2x+y-z=0 3. Solve the following linear system using the Gaussian elimination method. 4x-5y=-6...

-

Adam is 38 years old and has never been Benjamin, age 15, is Adam's nephew who lived with him all year. Adam provided all of Benjamin's supp and provided over half the cost of keeping up the home. ...

-

1. Which of the four major types of information systems do you think is the most valuable to an organization? 2. How do you critically associate the ideas of business agility and business efficiency...

-

Hardwood Furniture Ltd produces standard dining-room tables and chairs on a production line that includes a cutting department, a shaping department, a construction department and a finishing...

-

The accounts below are taken from the ledger of Bartel Music Consulting on 30 June 2016, the end of the current financial year. Required A. Record the closing entries which affected the accounts. B....

-

Now that we have adopted the perpetual inventory system, we no longer need to conduct a costly and time-consuming stocktake. Discuss.

-

T/F: BOs is the middle layer of stability model.

-

T/F: BOs are internally stable and externally adaptable.

-

T/F: BOs are the capabilities of achieving the goals (EBTs).

Study smarter with the SolutionInn App