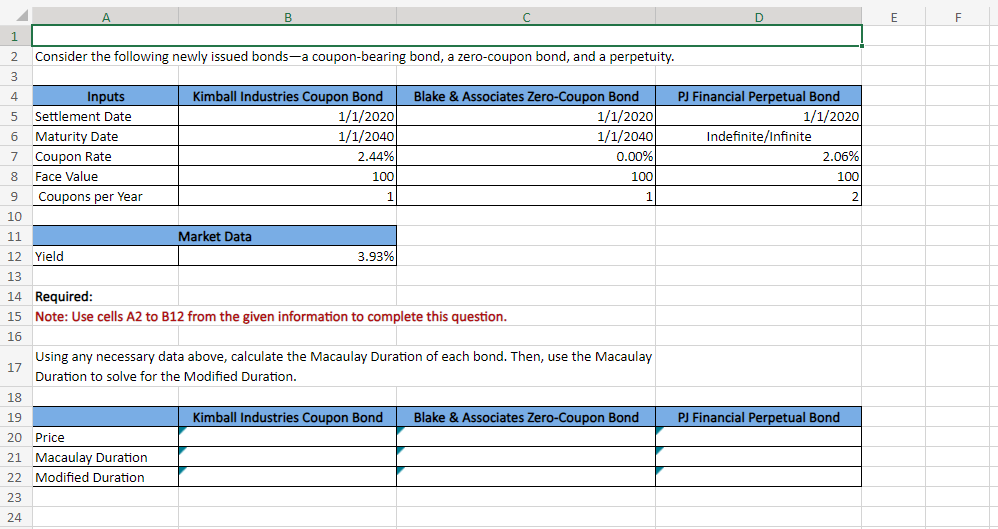

Question: B D E F 1 2 Consider the following newly issued bonds-a coupon-bearing bond, a zero-coupon bond, and a perpetuity. 3 4 Inputs Kimball

B D E F 1 2 Consider the following newly issued bonds-a coupon-bearing bond, a zero-coupon bond, and a perpetuity. 3 4 Inputs Kimball Industries Coupon Bond 5 Settlement Date 1/1/2020 Blake & Associates Zero-Coupon Bond 1/1/2020 PJ Financial Perpetual Bond 1/1/2020 6 Maturity Date 1/1/2040 1/1/2040 Indefinite/Infinite 7 Coupon Rate 2.44% 0.00% 2.06% 8 Face Value 9 Coupons per Year 100 1 100 100 1 2 10 11 Market Data 12 Yield 3.93% 13 14 Required: 15 Note: Use cells A2 to B12 from the given information to complete this question. 16 17 Using any necessary data above, calculate the Macaulay Duration of each bond. Then, use the Macaulay Duration to solve for the Modified Duration. 18 19 Kimball Industries Coupon Bond Blake & Associates Zero-Coupon Bond PJ Financial Perpetual Bond 20 Price 21 Macaulay Duration 22 Modified Duration 23 24

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts