Question: Based on historical data, you have estimated the following probability distributions for the returns on two individual securities (SMALL and BIG) and the value-weighted market

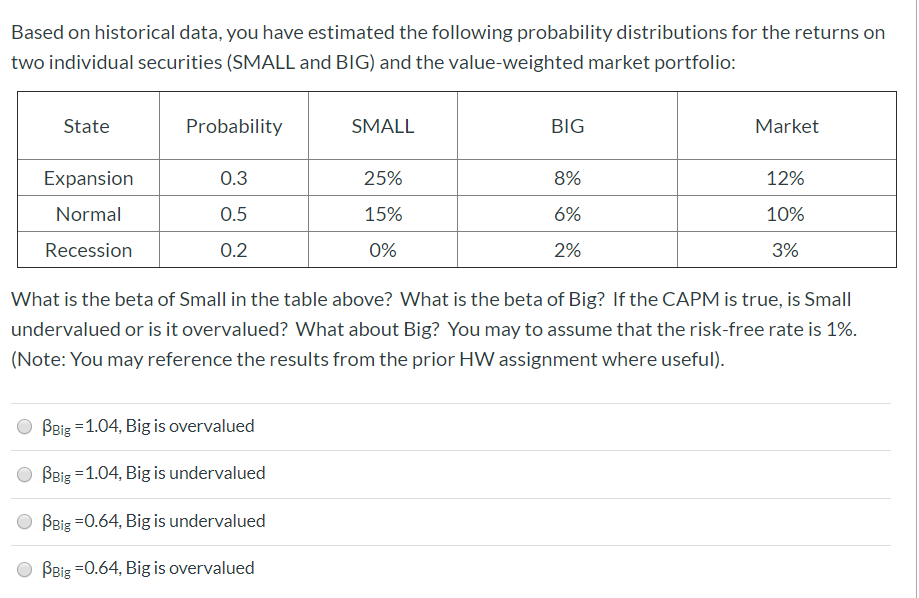

Based on historical data, you have estimated the following probability distributions for the returns on two individual securities (SMALL and BIG) and the value-weighted market portfolio: State Probability SMALL BIG Market Expansion 0.3 25% 8% 12% Normal 0.5 15% 0% 6% 2% 10% 3% Recession 0.2 What is the beta of Small in the table above? What is the beta of Big? If the CAPM is true, is Small undervalued or is it overvalued? What about Big? You may to assume that the risk-free rate is 1%. (Note: You may reference the results from the prior HW assignment where useful). BBig = 1.04, Big is overvalued O BBig =1.04, Big is undervalued OBBig =0.64, Big is undervalued BBig=0.64, Big is overvalued

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts