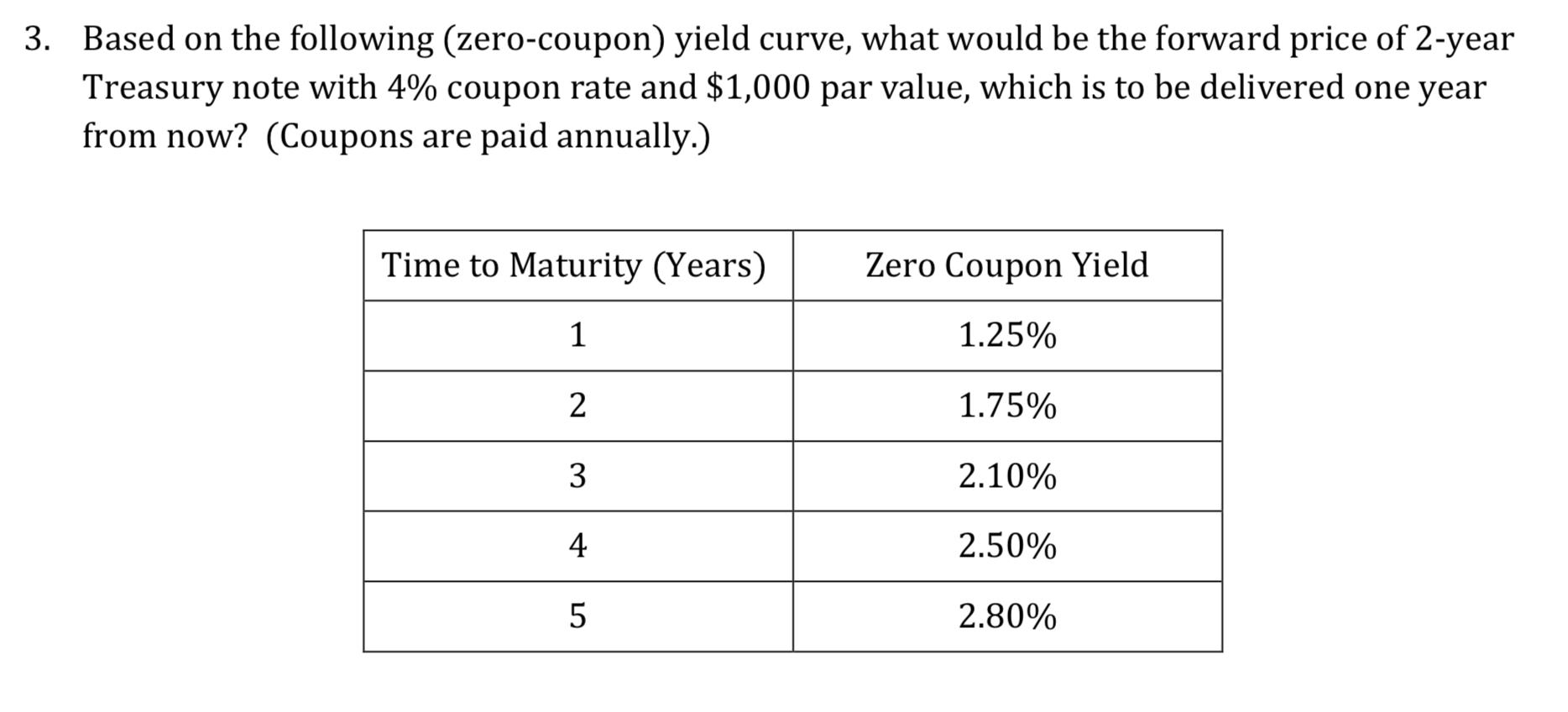

based on the following (zero-coupon) yield curve, what would be the forward price of 2-year treasury notes

Fantastic news! We've Found the answer you've been seeking!

Question:

based on the following (zero-coupon) yield curve, what would be the forward price of 2-year treasury notes with a 4% coupon rate and 1000 par value, which is to be delivered one year from now. (coupon is paid annually)

treasury notes with a 4% coupon rate and 1000 par value, which is to be delivered one year from now. (coupon is paid annually)

Expert Answer:

Related Book For

Niebels Methods, Standards and Work Design

ISBN: 978-0073376318

13th edition

Authors: Andris Freivalds, Benjamin Niebel

Posted Date: