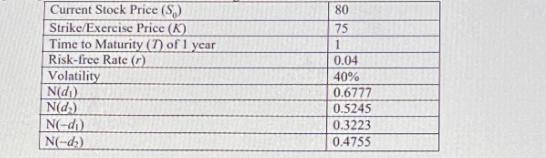

Based on the information and the Black-Scholes-Merton model, estimate Delta (A) of the European Put option. Current

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To estimate the Delta of a European Put option using the BlackScholesMerton model you can use the ... View the full answer

Related Book For

Introduction to Management Science A Modeling and Cases Studies Approach with Spreadsheets

ISBN: 978-0078024061

5th edition

Authors: Frederick S. Hillier, Mark S. Hillier

Posted Date: