Question: Boeing imported a Rolls-Royce jet engine for 10 million payable in three months. The current spot rate is $1.36/ and three-month forward rate is $1.3/.

Boeing imported a Rolls-Royce jet engine for 10 million payable in three months. The current spot rate is $1.36/ and three-month forward rate is $1.3/. A three-month put option on pounds with a strike price of $1.32/ has a premium of $0.015 per pound, while a three-month call option on pounds with the same strike price has a premium of $0.018 per pound . Currently, three-month interest rate is 3.2% per annum in the U.S. and 4.4% per annum in the U.K.

Boeing is considering alternative ways of hedging this foreign currency payable. It tries to minimize the dollar cost of paying off the payable. All questions below refer to cash flows in three months.

1. What would be the future dollar cost if Boeing decides to hedge using a forward contract? Indicate whether Boeing should use a long or short forward contract. How risky (certain/uncertain) is this cash flow?

Please note if below image is not visible, right click on the image and select option 'open in new tab', the image will open in new tab and could be enlarged for better visibility.

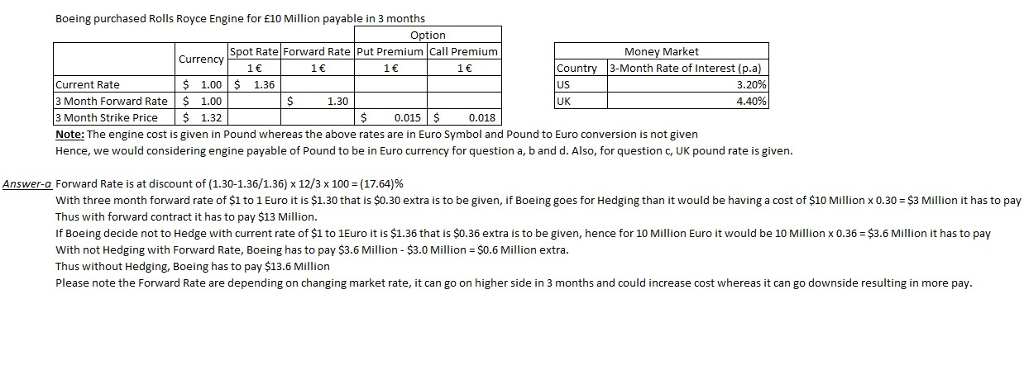

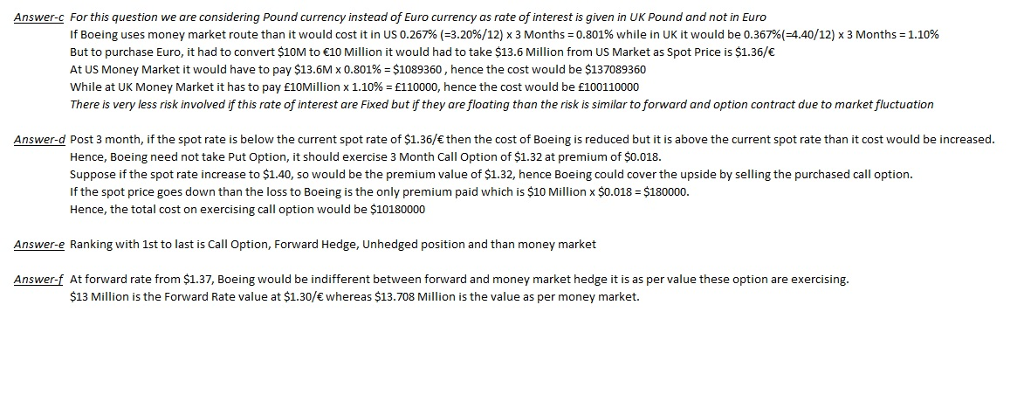

Boeing purchased Rolls Royce Engine for 10 Million payable in 3 months ion t Rate Forward Rate Put Premium Call Premium 1 Money Market Currency 1 1 1 Country 3-Month Rate of Interest (p.a) US UK 1.00 1.36 3.20% 4.40% Current Rate 3 Month Forward Rate $ 1.00 3 Month Strike Price 1.32 Note: The engine cost is given in Pound whereas the above rates are in Euro Symbol and Pound to Euro conversion is not givern Hence, we would considering engine payable of Pound to be in Euro currency for question a, b and d. Also, for question c, UK pound rate is given. 1.30 $0.0150.018 Answera Forward Rate is at discount of (1.30-1.36/1.36) x 123 x 100-(17.64)% With three month forward rate of $1 to 1 Euro it is $1.30 that is $0.30 extra is to be given, if Boeing goes for Hedging than it would be having a cost of $10 Million x 0.30 $3 Million it has to pay Thus with forward contract it has to pay $13 Million. If Boeing decide not to Hedge with current rate of $1 to 1Euro it is $1.36 that is $0.36 extra is to be given, hence for 10 Million Euro it would be 10 Million x0.36 $3.6 Million it has to pay With not Hedging with Forward Rate, Boeing has to pay $3.6 Million $3.0 Million $0.6 Million extra. Thus without Hedging, Boeing has to pay $13.6 Million Please note the Forward Rate are depending on changing market rate, it can go on higher side in 3 months and could increase cost whereas it can go downside resulting in more pay

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts