Question: Both bonds pay interest annually. The current benchmark for the 3-year EUR interest rate swap is 2.12%. What is the G-spread in basis points for

Both bonds pay interest annually. The current benchmark for the 3-year EUR interest rate swap is 2.12%.

What is the G-spread in basis points for UK corporate bonds?

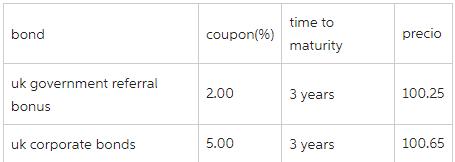

bond uk government referral bonus uk corporate bonds coupon(%) 2.00 5.00 time to maturity 3 years 3 years precio 100.25 100.65

Step by Step Solution

★★★★★

3.56 Rating (153 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To calculate the Gspread in basis points for UK corporate bonds we need to compare their yield to th... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock