Question: (c) Now consider a convertible bond that is issued by firm ABC at t=0 at a face value of 100 with a maturity of 1

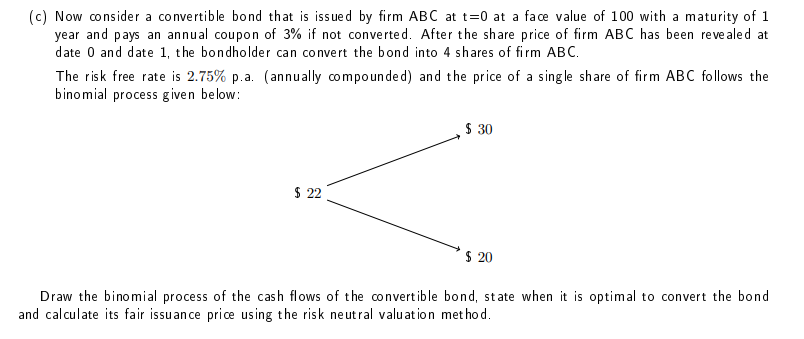

(c) Now consider a convertible bond that is issued by firm ABC at t=0 at a face value of 100 with a maturity of 1 year and pays an annual coupon of 3% if not converted. After the share price of firm ABC has been revealed at date 0 and date 1 , the bondholder can convert the bond into 4 shares of firm ABC. The risk free rate is 2.75% p.a. (annually compounded) and the price of a single share of firm ABC follows the binomial process given below: Draw the binomial process of the cash flows of the convertible bond, state when it is optimal to convert the bond and calculate its fair issuance price using the risk neutral valuation method. (c) Now consider a convertible bond that is issued by firm ABC at t=0 at a face value of 100 with a maturity of 1 year and pays an annual coupon of 3% if not converted. After the share price of firm ABC has been revealed at date 0 and date 1 , the bondholder can convert the bond into 4 shares of firm ABC. The risk free rate is 2.75% p.a. (annually compounded) and the price of a single share of firm ABC follows the binomial process given below: Draw the binomial process of the cash flows of the convertible bond, state when it is optimal to convert the bond and calculate its fair issuance price using the risk neutral valuation method

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts